Why Your Marketing Agency Is Profitable on Paper But Always Short on Cash

You just closed your best quarter ever for your agency. Three new retainers signed, a project invoice sent for more than you billed in all of January, and your P&L looks like something you would frame and hang on the wall.

Then your bank account sends a different message entirely.

Payroll is in six days. Two clients are sitting at 75 days past due. Your bookkeeper is asking about HST remittances. And the number in your chequing account does not match any version of reality your accountant has shown you.

This is not a revenue problem. It is not even really a cash flow problem, at least not in the way most accountants diagnose it. It is a structural problem, specific to how agencies earn money and how that timing collides with how agencies spend it.

There are three financial mechanics that make agencies uniquely vulnerable to this gap. Most agency founders do not know the names for them. Most generalist accountants do not think to look for them. Here is a clear-eyed breakdown of each, why it happens, and what fixing it actually looks like.

You are not alone in this. According to the Zenbooks Technology in Accounting study, conducted across 500 Canadian SME owners, 34% of small business owners said managing cash flow causes them at least a moderate headache, making it one of the top two financial pain points reported, tied only with paying bills. Yet only 9% of those using an external accounting provider said that provider delivers cash flow projections. The gap between the problem and the service being delivered is enormous.

Agency 1: Project Billing Cycles Create a Revenue Recognition Lag

When a product company sells something, the transaction and the revenue are the same moment. You sell, you collect, done.

Agencies do not work that way. An agency sells time and expertise in advance, often in large project blocks, and then delivers that value over weeks or months. The invoice might go out on day one. The work happens over the next 60 days. The client pays on net 30 or net 60 terms from the invoice date. By the time the cash arrives, the people who did the work have already been paid twice.

This creates a structural lag between earning and collecting that compounds with scale. The more revenue you add, the wider the gap gets, because you are always funding a larger and larger forward delivery commitment with cash from projects that closed last quarter.

The accounting jargon of this problem is revenue recognition. Under accrual accounting, which is the correct method for any agency doing more than a few hundred thousand dollars in revenue, you cannot book revenue when you invoice. You book it when you earn it, as the work is delivered. This means your P&L might show $200,000 in earned revenue in a month where you collected $80,000 in cash and spent $160,000 in salaries and overhead.

Profitable on paper. Negative in the bank.

The fix is not to change your billing terms overnight, though tightening them does help….. The fix is to separate your revenue picture from your cash picture, and to stop using your P&L as a proxy for either. An accrual-based income statement tells you whether the business is economically sound. It does not tell you whether you can make payroll on Thursday.

Agency 2: Deferred Revenue Gets Misclassified, and the Books Lie to You

This is the one we see most often when we onboard a new agency client. It is also the one that causes the most surprise.

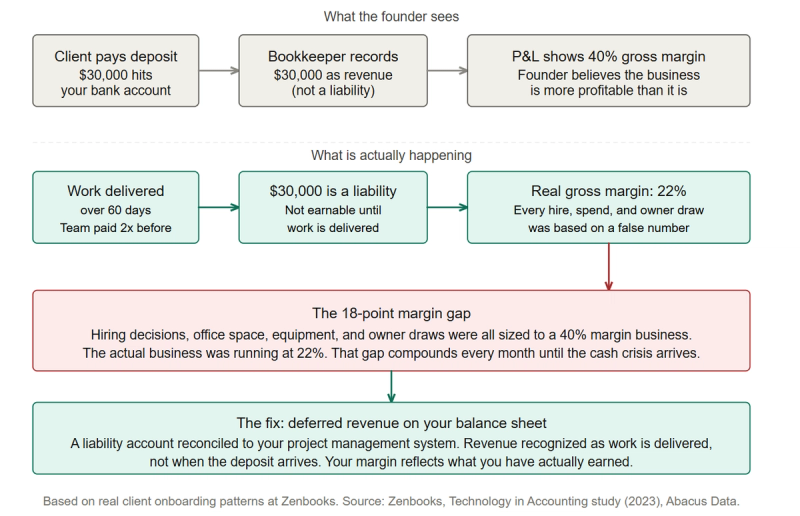

When a client pays you a deposit, or prepays for a retainer block, that money hits your bank account and feels like income. It is not. It is a liability. You owe that client work. Until you deliver the work, the cash sitting in your account belongs to a commitment you have not yet fulfilled.

If your bookkeeper records that deposit as revenue when it arrives, your books show higher income than you have actually earned. Your tax bill reflects earnings you have not yet realized. Your gross margin looks healthier than it is. And your sense of how much cash you can spend is dangerously inflated.

We have seen agencies running at what they believed was 40% gross margin discover, after proper deferred revenue accounting is applied, that their real margin was closer to 22%. The business was not failing. But every financial decision the founder had been making, on hiring, on space, on equipment, on their own draw, was based on a number that was not real.

Fixing deferred revenue misclassification requires a clean liability account on your balance sheet, systematic recognition as work is delivered, and a regular reconciliation against your project management system. It is not complicated work. But it requires a bookkeeper and accountant who understand how agency revenue actually moves, not just how to categorize deposits in a general ledger.

The Zenbooks Technology in Accounting study found that only 32% of Canadian SME owners reported being very satisfied with how their accounting and bookkeeping are currently handled. Among growth-oriented owners actively trying to scale, that number drops to 24%. When your books are misstating your margin by 18 percentage points, as in the example above, that dissatisfaction is not a service complaint. It is a structural one.

Agency 3: Media Buying Float Is Agency Cash in Disguise

Not every agency deals with this one, but for those running paid media campaigns on behalf of clients, it is worth understanding clearly.

When your agency books media placements, you often pay the platform, the publisher, or the vendor upfront. Facebook, Google, programmatic networks, and most traditional media buys require payment before the campaign runs. Your client then reimburses you, on whatever terms you have negotiated, which is rarely the same day you advanced the cash.

The gap between what you pay out and what you collect back is called media float. At low volumes it is manageable. At $50,000 a month in media spend, you are routinely carrying a five-figure advance on behalf of clients while also funding your own operations. At $200,000 a month, that number starts affecting your ability to make hiring decisions, investment decisions, and sometimes payroll decisions.

The accounting solution here is to track media spend separately from agency revenue and cost, to reconcile client media budgets monthly, and to build your cash flow projections in a way that accounts for the timing difference. Agencies that do not do this often cannot tell you, in any given week, how much of the cash in their account is actually theirs versus money they are holding temporarily for a client campaign.

What Proper Agency Finance Actually Looks Like

Each of these three agencies have a named solution. Taken together, they describe what a properly constructed agency finance function should be producing for you every month.

The same study found that among Canadian SMEs using an external accounting provider, only 6% said their provider conducts a monthly check-in call, and only 32% said their provider handles monthly bookkeeping. The majority are getting year-end tax compliance and nothing else. For an agency managing billing cycles, deferred revenue, and media float simultaneously, year-end-only accounting is not just insufficient. It means every financial decision between January and December is being made without a finance partner in the room.

You should receive an accrual-based P&L that reflects earned revenue, not billed revenue. Your balance sheet should carry a deferred revenue liability account that reconciles to your project management system. Your cash flow reporting should separate operating cash from media float if you run client campaigns. And you should have a forward-looking cash projection, at minimum a 13-week rolling model, that tells you not just where cash is today but where it will be when your next large payroll runs, your next HST remittance is due, and your slowest-paying client finally settles.

This is not fractional CFO territory. It is not complicated. It is what any well-structured agency accounting function should be producing as a baseline, and it is the difference between knowing your numbers and being surprised by them.

Joy Hawkins, founder of Sterling Sky, a Canadian SEO agency, has worked with Zenbooks to manage exactly this kind of complexity as her firm has grown. Marie Haynes of Marie Haynes Consulting, another Ottawa-based SEO agency, has credited Zenbooks with supporting her firm's growth from a solo practice to a team of ten, handling accounting, bookkeeping, and payroll as the business scaled. You can read more about the agencies and professional services firms we work with by checking out our case studies.

Frequently Asked Questions

What is the difference between cash flow and profitability for a marketing agency?

Profitability is whether your revenue exceeds your costs over a given period, measured on an accrual basis. Cash flow is whether you have enough money in the bank to meet your obligations when they are due. An agency can be consistently profitable on an accrual P&L and still run out of operating cash if the timing between delivering work, invoicing clients, and collecting payment is misaligned. These are two separate measurements and they require two separate reports.

What is deferred revenue and why does it matter for agencies?

Deferred revenue is cash you have collected from a client for work you have not yet delivered. It is a liability, not income. If your accounting system records client deposits or retainer prepayments as revenue when received, your books are overstating your earnings and understating your obligations. This leads to inflated margin calculations, incorrect tax reporting, and financial decisions made on numbers that do not reflect reality.

What is a 13-week cash flow model and do agencies need one?

A 13-week rolling cash flow model projects your expected cash inflows and outflows across the next 13 weeks on a week-by-week basis. It accounts for when client payments are actually expected to land based on invoice dates and payment terms, not when revenue is earned. For agencies managing project-based billing, client payment lag, and lumpy payroll timing, a 13-week model is the only tool that gives you an accurate picture of whether you will have enough cash on hand at any specific future date.

How do I know if my deferred revenue is being tracked correctly?

Check your balance sheet. There should be a liability line item labelled deferred revenue or unearned revenue that corresponds to client deposits and prepaid retainers. If that line does not exist and your firm routinely collects deposits or monthly retainers in advance, your books are likely recording prepayments as revenue incorrectly. A qualified accountant familiar with project-based service businesses can reconcile this quickly.

What does an agency accounting firm do differently than a general bookkeeper?

A general bookkeeper records transactions. An accountant familiar with the agency model will structure your chart of accounts to separate media spend from agency revenue, build a deferred revenue liability account, implement accrual recognition policies, and produce cash reporting alongside your P&L. The difference is not just accuracy. It is whether your reporting is actually decision-useful or just a compliance document.

Is Zenbooks a good fit for marketing and creative agencies?

Zenbooks works with founder-led Canadian agencies in the $1M to $10M revenue range. If you are at that stage and want a finance team that understands project billing cycles, deferred revenue, and forward-looking cash reporting, we are likely a strong fit. If you are below $1M or above $10M, we will tell you honestly and point you in the right direction. You can learn more here.

The Bottom Line

Your P&L is not lying to you. It is just answering a different question than the one you need answered on the day you are short on cash.

The gap between profitable and liquid is not a mystery. It has specific names: billing cycle lag, deferred revenue misclassification, and media float. Each one is measurable, each one is manageable, and none of them require a CFO to fix. They require an accounting function that understands how agencies actually earn money.

If you are not sure which of these mechanics is driving your cash gap, the Zenbooks Financial Clarity Assessment takes two minutes and will show you where your financial infrastructure has gaps. If you already know what you need, book a free consultation and we can talk through what a properly structured agency finance function would look like for your business.

Jessica Wong, CPA, CA, leads operations and accounting services at Zenbooks, where she helps growing Canadian businesses get accurate books, practical insights and a better client experience.

Subscribe for Updates

Business Clarity That Helps You Breathe Easy

Achieve your business goals and peace of mind with Zenbooks. As both your finance team and business advisor, we empower you every step of the way.