Cash Flow for Marketing Agencies: What Your Accountant Should Be Telling You (But Probably Isn't)

If you run a founder-led marketing or creative agency in Canada, there is a good chance your accountant shows up once a year, hands you a tax return, and calls it a year. Maybe they file your HST. Maybe they answer the occasional panicked question about a CRA notice.

What they are probably not doing is helping you understand why your cash position feels so precarious even when your agency is busy, growing, and signing retainer clients.

That is not a minor gap. For agencies running on retainer models, project-based billing, and scope-heavy client relationships, the difference between good cash flow management and bad cash flow management is often the difference between scaling confidently and quietly drawing on your line of credit every quarter just to make payroll.

Here is what your accountant should be telling you.

The Retainer Model Feels Safe. It Is Not Automatically Safe.

Retainers are the holy grail for agency owners. Predictable revenue. Recurring relationships. Less time pitching. All true. But retainers introduce a specific set of cash flow risks that most generalist bookkeepers are simply not equipped to flag.

The core problem is timing. When a client signs a retainer and you collect payment upfront, that money is not yet income. It is a liability. You have been paid for work you have not done. If you record it as revenue immediately and spend accordingly, you are running on cash that is not yet earned.

This is deferred revenue, and it is foundational to how agency finances should work. A proper accrual-based accounting setup recognizes revenue only when the work is performed, not when the invoice is paid. For a retainer client paying $10,000 per month three months in advance, that is $30,000 sitting on your balance sheet as a liability until your team actually delivers.

Most agency founders have never had this explained to them. According to our national research study on technology in accounting, only 9% of Canadian SMEs working with an external provider receive cash flow projections as part of the service. Nine percent. If your accountant is not proactively modelling how your deferred revenue balances affect your real cash position month over month, you are operating with incomplete information.

"We see this constantly with agencies that come to us after outgrowing a generalist bookkeeper. The books look clean. The P&L looks fine. And then we pull the deferred revenue schedule and the real picture is completely different from what the founder thought they had."

— Colin Robinson, Principal, Zenbooks

Scope Overflow Is a Cash Flow Problem, Not Just a Billing Annoyance

Every agency owner knows the feeling. A client asks for "one small thing" that turns into a full extra deliverable. Your team absorbs it. The project wraps. The invoice goes out for the original scope. And somewhere in the back of your mind you know you just gave away margin you never had. But you are trying to build goodwill and make the client happy.

Scope overflow is not just a project management failure. It is a cash flow problem with compounding effects.

When unbilled work accumulates, your revenue recognition falls out of alignment with your actual effort. You may be working at 110% capacity and showing strong booked revenue while your realized cash per hour collapses. I know this because I handle the day to day operations for Zenbooks too! The income statement looks fine. The bank account tells a different story. When you need to increase fees, you hope the client remembers that time months or years ago when you did a few things not explicitly listed in the scope. They usually do not.

A proactive accounting firm should be flagging this. They should be reviewing your work-in-progress positions, identifying patterns in scope creep across clients, and helping you build the language and systems to catch and bill overages in real time, not six weeks after the fact.

Moniker Partners, a corporate travel and retreat planning company that grew from $5M to over $20M in four years, came to Zenbooks after a previous accounting firm let deferred revenue tracking slide, left accounts receivables disorganized, and failed to build consistent month-end close processes. The result was financial blind spots at exactly the moment rapid growth made those blind spots most dangerous. Read the full Moniker case study.

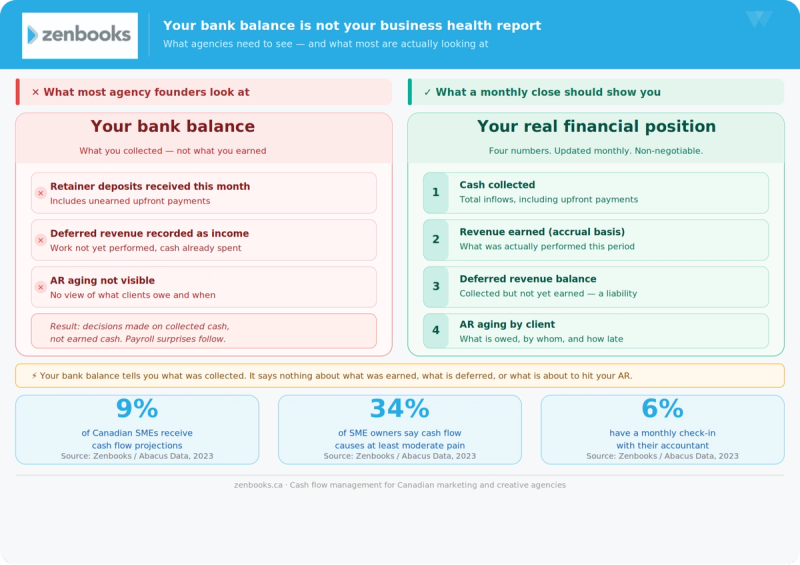

Your Bank Balance Is Not Your Business's Health Report

This is the most dangerous habit we see in founder-led agencies: checking the bank account to assess financial health.

Your bank balance tells you what has been collected. It says nothing about what has been earned, what is owed, what is deferred, or what is about to hit your AR aging. On a good retainer month where three clients paid upfront, your balance looks excellent. On the month those retainers are worked down and no new clients have signed, the reality arrives fast.

What you actually need is a real-time view of four things: cash collected, revenue earned (accrual), deferred revenue balance, and AR aging by client. A proper monthly close should deliver all of this to you before you make any operational decisions. Hiring decisions, new hires, equipment purchases, owner draws: all of these should be made against your earned cash position, not your collected cash position.

The research bears this out. Our Zenbooks study conducted with Abacus Data found that managing cash flow is one of the top financial headaches for Canadian SMEs, with 34% of business owners reporting it causes at least moderate pain. And yet traditional accounting firms, as the same study shows, rarely offer the proactive advisory services that would actually address it.

The Upfront Recognition Problem Nobody Talks About

Here is a scenario that plays out in agencies constantly. A client signs a $60,000 annual contract. They pay the first $30,000 upfront. You recognize the full $30,000 as revenue in month one.

Your accountant does not flag this. Your bookkeeper records the deposit. Your P&L looks strong. You hire.

Then the work gets delivered over the next six months. New revenue does not materialize as expected. Now you have a team staffed to a revenue level that was never real. The $30,000 you spent was spoken for before it was earned, and you have no financial model showing you what the earned revenue trajectory actually looked like.

This is the upfront recognition problem. It is especially acute for agencies signing large annual retainers or multi-phase project contracts. The fix is not complicated: it requires an accounting setup that distinguishes between cash received and revenue earned, and a monthly reporting process that shows both.

If your accountant has never walked you through your deferred revenue balance or explained why it matters for your hiring decisions, that is a gap worth addressing. You can see what our clients say about how Zenbooks handles this -- and why the difference between a compliance-first firm and an advisory partner shows up most clearly in moments exactly like this one.

What Proactive Cash Flow Advisory Actually Looks Like

For context, here is what agencies working with a proactive accounting partner should be receiving as standard practice, not as a premium add-on.

A monthly close that closes on time. Not six weeks late, not whenever your bookkeeper gets around to it. If your books are not closed within two to three weeks of month end, you are always making decisions on stale information.

A cash flow forecast updated monthly. This does not need to be a sophisticated model. It needs to show inflows from existing retainers, expected AR collections, deferred revenue release, and upcoming payables. Four columns. Updated monthly. This alone would change how most agency founders make decisions.

A deferred revenue schedule. Every retainer, every upfront payment, every multi-month project should appear on a schedule showing when that revenue is expected to be earned. Your bookkeeper should be maintaining this. Your accountant should be reviewing it.

A scope and billing review conversation. At least quarterly, your accounting partner should be asking about your largest clients, whether scope has crept, and whether your billing reflects the work actually being done. This is not accounting. It is advisory. It is also what separates a firm like Zenbooks from a firm that files your returns and disappears.

"The agencies that navigate growth without hitting a cash wall are not the ones with the best accountants. They are the ones where someone is actually looking at the numbers on a regular schedule and asking what they mean for decisions that have not been made yet."

— Eric Saumure, CPA, CA, Principal, Zenbooks

The Menos Example: What Getting This Right Looks Like

Menos, a cross-border e-commerce and Shopify app company that Zenbooks has worked with since 2018, started with $156,000 in annual revenue. By 2025 they exceeded $12 million. Part of that growth was product and market. But a significant part of it was having real-time financial infrastructure: bank and payment reconciliation done on a live basis, monthly leadership check-ins, weekly fractional CFO touchpoints, and a tech stack fully integrated so that financial data was never more than a few days old.

That level of financial clarity does not happen by accident, and it does not happen when your accountant only surfaces once a year. Read the full Menos case study.

You can also browse our full library of client case studies and client reviews to see how this plays out across different business types and growth stages.

Why This Is Especially Important for Canadian Agencies Right Now

The Canadian marketing services market is under real pressure. Clients are scrutinizing retainer renewals more carefully. AI is a real threat and opportunity. Project scopes are being compressed. Payment terms are stretching. In this environment, an agency that does not have granular visibility into its cash position is exposed in a way that would have been survivable two years ago but may not be today.

This is also the moment when the advisory gap in traditional accounting becomes most costly. The same Zenbooks research found that only 6% of Canadian SMEs working with an external provider have a monthly check-in with their accountant. Six percent. At a time when the financial environment for small businesses is as complex as it has been in years, the majority of business owners are navigating alone between annual tax filings.

If you are a marketing agency founder carrying retainer clients, running project-based billing, or managing a team of five or more people, you should not be in that 94%.

Frequently Asked Questions

What is deferred revenue and why does it matter for my agency?

Deferred revenue is money you have collected from a client for work you have not yet performed. Under proper accrual accounting, it sits as a liability on your balance sheet, not as income, until the work is done. For retainer-based agencies, this distinction is critical because it affects your real earned income position, your profitability per client, and your ability to make sound hiring and operational decisions.

How is cash flow different from profit?

Profit is your revenue minus your expenses, measured on an accrual basis. Cash flow is the actual movement of money in and out of your bank account. An agency can be highly profitable on paper while experiencing serious cash crunches if clients pay slowly, retainers are front-loaded, or payroll timing does not align with collections. Managing both requires different tools and a different kind of accounting support.

My bookkeeper handles my accounts. Is that enough?

A bookkeeper records transactions. That is valuable and necessary, but it is not cash flow management. Cash flow management requires a forward-looking perspective: forecasting, deferred revenue tracking, scope billing reviews, and advisory conversations about what the numbers mean for your business decisions. If your only financial support is reactive transaction recording, you have a gap.

How often should I be reviewing my cash position?

At minimum, monthly, against a closed set of books. For agencies above $1M in revenue with active retainer clients, a rolling 13-week cash flow forecast reviewed weekly is a meaningful step up. You do not need to obsess over it daily, but you do need a structured cadence that is tied to real, closed financial data rather than bank balance spot-checks.

When does it make sense to bring in a fractional CFO?

Generally, when you are above $2M in revenue, managing multiple retainer clients with complex billing arrangements, considering a significant hire, or exploring a capital raise or ownership transition. A fractional Controller brings the forward-looking financial strategy that sits above day-to-day bookkeeping and even standard accounting. At Zenbooks, we embed fractional Controller work directly into client relationships when the complexity warrants it.

What should I ask a potential accounting firm to see if they are a good fit for my agency?

Ask them how they handle deferred revenue for retainer-based businesses. Ask them what a monthly close looks like and how long it takes. Ask whether they will provide a cash flow forecast and how often it is updated. Ask whether they schedule a monthly call. The answers will tell you quickly whether you are talking to a compliance-first firm or an advisory partner. For a full breakdown of what to look for, see our post What to Actually Look for in an Accountant for Your Creative Agency.

If any of this resonates, you are not alone and you are not stuck. The gap between what most agencies receive from their accountant and what they actually need is real, and it is closable. Book a complimentary consultation with the Zenbooks team and we will walk you through what your financial picture actually looks like, and what it should look like.

Colin Robinson is co-founder and Principal of Zenbooks, which he built starting in 2015 into one of Canada's leading cloud accounting firms for small and mid-sized businesses. He leads Zenbooks' CFO advisory practice, working directly with founders and executive teams on financial strategy, cloud migration, and the kind of complex, non-standard situations that fall outside the playbook.

Before co-founding Zenbooks, Colin worked at Ernst & Young, one of the world's leading professional services firms. He holds a Bachelor of Commerce in Accounting.

Over a decade building and running Zenbooks, Colin has advised hundreds of Canadian entrepreneurs, from solo founders scaling past their first million to established businesses navigating ownership transitions and operational restructuring. His commentary on small business financial strategy has appeared in Le Droit.

Subscribe for Updates

Business Clarity That Helps You Breathe Easy

Achieve your business goals and peace of mind with Zenbooks. As both your finance team and business advisor, we empower you every step of the way.