How to Choose an Accountant for Your Professional Services Firm in Canada

If you run an engineering firm, management consulting practice, law firm, or architecture studio in Canada, your accounting needs are not the same as a retailer's or a restaurant's. You operate through a professional corporation governed by rules your accountant needs to have actually read. You carry shareholder loan balances that CRA monitors closely. You have holding company structures, compensation planning decisions, and governing body compliance requirements layered on top of the standard small business tax picture.

And yet, most professional services firms are working with a generalist accountant who learned about their industry on the job, at the firm's expense.

At Zenbooks, we work with professional services firms across Canada, and the patterns we see are consistent. The firms that outgrow their accountant fastest are usually the ones that never questioned whether their accountant was the right fit to begin with. This post is meant to change that.

Why Professional Services Firms Are a Different Accounting Problem

The core issue is layered compliance. Your firm does not just answer to the Canada Revenue Agency. It answers to a professional governing body whose rules interact with your corporate structure in ways a generalist accountant may not understand at all.

In Ontario, an engineering firm operating through a corporation must obtain a Certificate of Authorization from Professional Engineers Ontario before it can legally offer engineering services through that entity. A law professional corporation is subject to detailed ownership restrictions under the Law Society of Ontario, including rules about which family members can hold shares and under what conditions a holding company can be introduced into the structure. A medical or dental professional corporation has its own governing body requirements through the relevant College, many of which differ meaningfully from those that apply to lawyers or engineers.

These are not minor technicalities. Getting the share structure wrong at incorporation, or failing to maintain compliance with your governing body's ongoing requirements, creates regulatory risk that sits entirely outside the tax file. An accountant who has never worked with a regulated profession will give you technically accurate tax advice wrapped inside a structure that violates your governing body's rules. You will not find out until it becomes a problem.

"The first question I ask any professional services firm that comes to us is whether their accountant has experience with their governing body and their industry," says Jessica Wong, CPA, CA, Director of Operations at Zenbooks. "You’d be surprised how often the answer is no. That gap is usually where we find the most significant planning problems.."

The Professional Corporation Is a Planning Platform, Not Just a Tax Vehicle

Most incorporated professionals understand that their PC offers tax deferral on income retained inside the corporation. What many do not fully use is everything else the structure makes possible.

The PC is a compensation flexibility tool. As the shareholder-operator, you control the mix of salary and dividends you draw, which determines your RRSP contribution room, your CPP accumulation, your ability to fund a spousal RRSP, and your eligibility to claim childcare expenses through the lower-income spouse. Each of these decisions compounds over time in ways that make the annual tax bill question look small by comparison.

The PC is also a holding company feeder. Retained earnings inside your operating company can be moved to a holding company through tax-free intercorporate dividends, where they are protected from the creditors of the operating entity and can be invested or distributed on a flexible timeline. The holding company structure also plays a role in preserving the Lifetime Capital Gains Exemption, currently $1,250,000 on the sale of Qualified Small Business Corporation shares, by keeping the operating company's asset base sufficiently active.

If you want to assess if a holding company is right for your structure, you can try our holdCo analyser tool.

And the PC is an estate and succession planning tool. The share structure you set up today, including what classes of shares exist, who holds them, and how voting and economic rights are allocated, determines how easily the practice can be transitioned, sold, or wound down in the future.

If the primary touchpoint with your current accountant is a meeting in spring to review a year that is already over, you are paying for compliance and calling it advice. Those are not the same thing, and the gap compounds every year you do not close it. Our national study of 500 Canadian SMEs, conducted with Abacus Data, found that only 6% of business owners who work with an external accounting provider receive a regular monthly check-in. For a professional services firm with shareholder loan exposure, governing body compliance requirements, and compensation planning decisions to make every year, that cadence is not a preference. It is the difference between catching issues and cleaning them up.

An accountant who treats your PC as a mechanism to pay slightly less tax each year is leaving most of the value on the table.

The Shareholder Loan Problem Nobody Warns You About

Professional services firms accumulate shareholder loan balances more readily than most business types. The reasons are predictable: project-based billing creates lumpy cash flow, owner draws happen before the year-end tax picture is clear, and the line between corporate and personal spending gets blurry when the business is small and owner-operated.

Under section 15(2) of the Income Tax Act, if your corporation makes a loan to you as a shareholder and that loan is not repaid within one year after the end of the corporation's fiscal year in which the loan was made, the full amount of the loan is included in your personal income for the year the loan was made. That means potential double taxation: the corporation already paid tax on those earnings, and now you pay personal tax on the same dollars.

The situations that create shareholder loans are often mundane: draws taken before salary or dividends are formally declared, a cottage renovation paid through the corporate account, a personal vehicle purchased using corporate funds, or a home loan that flows through the corporate books. Each of these is legitimate under the right conditions and a tax problem under the wrong ones. The distinction comes down to documentation, intent, timing, and whether the repayment was part of a series of loans and repayments that CRA treats as a single ongoing balance rather than genuine repayment.

Holding company structures add another layer. Intercompany loans between an operating company and a related holding company need to be properly documented and priced at arm's length rates, and the attribution rules around income earned on loaned funds apply in ways that a generalist accountant may not flag proactively.

Your accountant should be reviewing the shareholder loan account balance at every reporting period, not surfacing it as a problem at year-end when the options to fix it have narrowed significantly.

Client #1: An Engineering Firm That Outgrew Its Accountant Slowly, Then All at Once

Consider a structural engineering principal based in Ontario running a firm with three licensed engineers and roughly $1.8M in annual billings. The firm had used the same general practice accountant for six years. The relationship was fine: tax returns filed on time, no CRA issues, annual meeting in April to review the prior year.

What the accountant had never flagged: the shareholder loan balance had been creeping upward for three years as the principal drew cash ahead of year-end dividend declarations. By the time the balance crossed $90,000, it was generating a deemed interest benefit that was showing up on the principal's personal return without a clear explanation of why. The holding company the accountant had set up was also structured with share ownership provisions that did not align with the firm's Certificate of Authorization requirements under Professional Engineers Ontario, a compliance issue that had existed since incorporation and that no one had noticed because no one had checked.

Untangling both issues required a combination of retroactive compensation adjustments, amended returns, and a corporate restructuring process that was significantly more expensive than proactive planning would have been.

Client #2: A Consulting Group That Asked the Right Questions Early

A management consulting group with two principals and $2.4M in annual revenue came to Zenbooks after their prior accountant left public practice. Rather than defaulting to the nearest available firm, they used the transition as an opportunity to evaluate what they actually needed.

They asked four questions in their first meeting with us: what professional services firms have you worked with, what does monthly reporting look like in practice, who is our primary contact and what is the response time commitment, and how do you handle year-end compensation planning for a two-principal structure with different income needs.

Those four questions revealed more about fit than any proposal document would have. They are now 18 months into the relationship. Their shareholder loan balances are reviewed monthly. Their compensation structures are modeled before the fiscal year ends rather than after. And the holding company structure they were considering is being built in the right sequence, with the governing body compliance question answered before the corporate documents are filed.

What a Good Accounting Relationship Actually Looks Like

The relationship model matters as much as the technical competence. For a professional services firm at the $1M to $5M revenue stage, the right accounting relationship looks like this: a monthly reporting package that you receive without chasing, a standing quarterly call to discuss what the numbers mean and what decisions they should inform, and a year-end planning conversation that happens before the fiscal year closes, not after.

The year-end conversation in particular should cover compensation mix (salary versus dividends, RRSP room targets, CPP calibration), shareholder loan balance management, any holding company dividend or investment decisions, and whether the corporate structure still fits the firm's current size and plans.

If the primary touchpoint with your current accountant is a meeting in spring to review a year that is already over, you are paying for compliance and calling it advice. Those are not the same thing, and the gap compounds every year you do not close it.

Professional services firms accumulate shareholder loan balances more readily than most business types. The reasons are predictable: project-based billing creates lumpy cash flow, owner draws happen before the year-end tax picture is clear, and the line between corporate and personal spending gets blurry when the business is small and owner-operated. The Zenbooks Technology in Accounting study found that while 34% of Canadian SMEs rank cash flow management among their top financial headaches, only 9% of those using an external accountant receive cash flow projections as part of the service. The gap between the problem and the support is exactly where shareholder loan balances creep up unnoticed.

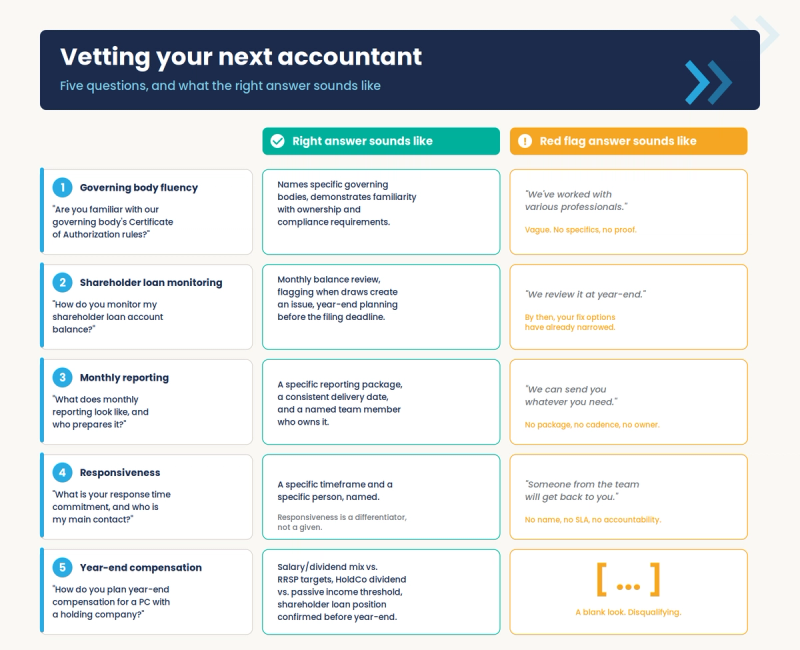

The Questions to Ask Before You Sign an Engagement Letter

Five questions that reveal whether a prospective accountant has genuine depth in professional services, along with what the right answer looks like:

"What regulated professions have you worked with, and are you familiar with the Certificate of Authorization requirements for our governing body?" The right answer names specific governing bodies and demonstrates familiarity with the ownership and compliance requirements. A vague answer about working with "various professionals" is not a right answer.

"How do you handle shareholder loan monitoring for owner-operated firms?" The right answer describes a proactive process: monthly review of the loan account balance, flagging when draws are creating a potential issue, and year-end planning to ensure the balance is addressed before the filing deadline. "We review it at year-end" is not a right answer.

"What does monthly reporting look like for a firm our size, and who prepares it?" The right answer describes a specific package, a consistent delivery date, and a named team member who owns it. "We can send you whatever you need" is not a right answer.

"What is your response time commitment and who is my primary point of contact?" The right answer gives a specific timeframe and a specific person. Responsiveness is a differentiator, not a given. If the answer is vague, that is useful information.

"How do you approach year-end compensation planning for a professional corporation with a holding company?" The right answer describes a structured process: reviewing the salary and dividend mix against RRSP targets, modeling the holding company dividend decision against the passive income threshold, and confirming the shareholder loan position before year-end closes. A blank look is a disqualifying answer.

You can review client experiences with our team at our Zenbooks reviews page or through the Moniker Partners case study, which documents a professional services firm that grew 4x in four years after restructuring their financial foundation.

Switching Accountants Is Less Disruptive Than Staying With the Wrong One

The most common reason professional services firms stay with an accountant who has stopped adding value is inertia. The relationship feels fine. The returns get filed. Nothing is on fire.

What that framing misses is the cost of what is not happening: the shareholder loan that is never flagged, the compensation structure that is never optimized, the holding company that is never built correctly, the governing body compliance question that is never asked.

For a $2M professional services firm, two or three years of that gap is a six-figure cost hiding inside a relationship that feels adequate. Switching firms requires 60 to 90 days of transition, a clean file handover, and a structured onboarding process. It is a project, not a crisis.

If you want to understand where your firm stands before making any decisions, the Zenbooks Financial Clarity Assessment takes two minutes and gives you an immediate read on your financial management gaps. No obligation.

Frequently Asked Questions

What is the difference between a professional corporation and a regular corporation in Canada?

A professional corporation is governed by both the Ontario Business Corporations Act and the rules of the relevant professional governing body, such as Professional Engineers Ontario or the Law Society of Ontario. Shareholder eligibility is restricted to licensed members of the profession in most cases, and the corporation must obtain a Certificate of Authorization from its governing body before offering professional services through the entity. Regular corporations do not have these restrictions.

What are the shareholder loan rules for professional services firm owners in Canada?

Under section 15(2) of the Income Tax Act, a loan from your corporation to you as a shareholder must generally be repaid within one year after the end of the corporation's fiscal year in which the loan was made. If it is not repaid within that window, the full amount is included in your personal income for the year the loan was made. The loan must also bear interest at no less than the CRA prescribed rate, which is reviewed quarterly. Certain exceptions exist for loans made for specific purposes such as home purchase or share acquisition, but these require careful documentation.

Can I have a holding company alongside my professional corporation?

It depends on your governing body's rules. Some professions permit holding companies as shareholders of the professional corporation under specific conditions. For example, Law Society of Ontario rules allow holding companies as shareholders of law professional corporations provided the holding company's shareholders, directors, and officers are restricted to the relevant lawyers. Other professions have different or more restrictive rules. This question should be answered before any corporate structure is built, not after.

How often should my accountant be in contact with me as a professional services firm owner?

At minimum, you should receive a monthly reporting package, have a standing quarterly planning call, and have a dedicated year-end compensation review before your fiscal year closes. If your accountant's primary touchpoint is an annual tax meeting in spring, that is a compliance relationship, not an advisory one.

What is the most common accounting mistake professional services firms make?

Allowing the shareholder loan balance to accumulate without monitoring it against the one-year repayment rule. This happens most often when draws are taken before compensation is formally declared, personal expenses flow through the corporate account, or a holding company introduces intercompany transactions that are not properly documented. The fix is a monthly review process, not a year-end scramble.

How do I know if I need a new accountant?

If you only hear from your accountant at tax time, if your shareholder loan balance is never proactively discussed, if you have never had a year-end compensation planning conversation before your fiscal year closed, or if your accountant cannot answer a question about your governing body's rules, those are material gaps. The decision to switch should be evaluated against the cost of staying, which is rarely zero.

Jessica Wong, CPA, CA, is Director of Operations at Zenbooks, where she has led the firm's accounting services and client operations since 2020. She brings over a decade of experience working directly with small and mid-sized business owners, with a focus on building efficient financial processes, improving month-end close cycles, and translating complex numbers into clear operational insights.

Before joining Zenbooks, Jessica held senior accounting roles across the hospitality and professional services sectors, including Corporate Controller at Hawksworth Restaurant Group and Manager of Client Onboarding at a national cloud accounting firm. She began her career in public accounting at Crowe. She holds a Bachelor of Business Administration from Simon Fraser University and her CPA, CA designation.

Jessica's writing on accounting operations and the future of remote work has appeared in the Toronto Star.

Subscribe for Updates

Business Clarity That Helps You Breathe Easy

Achieve your business goals and peace of mind with Zenbooks. As both your finance team and business advisor, we empower you every step of the way.