How to Pay Yourself as a Marketing Agency Owner in Canada

You built the agency. You landed the clients, hired the team, survived the slow months, and now the corporation is generating real profit. The question you probably have not answered with any precision is: how should that money actually get to you?

Most agency owners we talk to have a number they picked somewhat arbitrarily, a salary that "feels reasonable," topped up with whatever cash is left over when the account looks healthy. That is not a plan. It is a default. And defaults have a compounding cost that shows up quietly over 10 to 20 years in the form of missing RRSP room, no CPP, no retirement savings in a spouse's hands, and a tax bill that was larger than it needed to be every single year.

This post is the framework we actually use with marketing and creative agency owners. Not a surface-level salary versus dividends summary, but the full sequencing: what to look at first, what tools most owners are not using, and how to build a compensation structure that works with your agency's cash flow rather than against it.

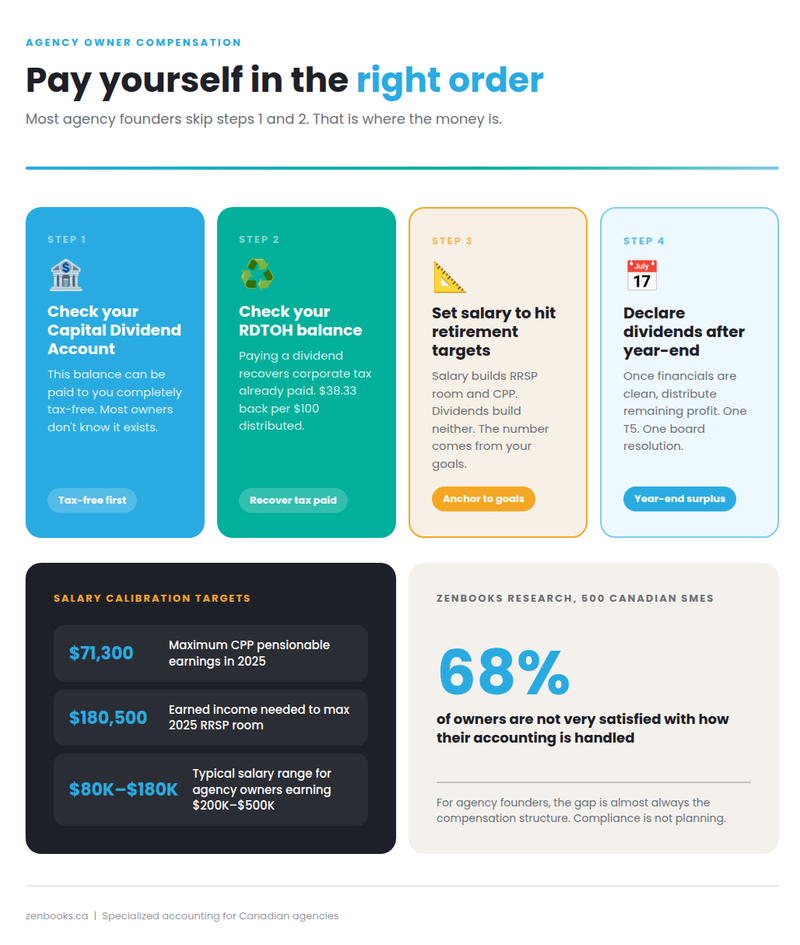

According to Zenbooks' national survey of 500 Canadian SMEs, only 32% of business owners report being very satisfied with how their accounting and bookkeeping are handled. For agency founders, the gap between satisfaction and optimization is almost always the compensation structure.

Why Agency Owners Need a Different Conversation

The standard small business compensation advice does not account for how agencies actually operate. Revenue is project-based. Retainers provide some stability, but most agencies experience meaningful peaks and valleys across the year. A $2M agency might collect $400K in one quarter and $180K in another. Personal expenses, however, are fixed: mortgage, childcare, groceries, insurance.

Drawing cash reactively whenever the account looks full is one of the most reliable ways to create a personal tax problem and a business cash flow problem simultaneously. The right structure separates your personal income from your agency's billing cycle entirely. Here is how to build it.

Step One: Check the Capital Dividend Account Before Anything Else

Before you model any salary or dividend mix, your accountant should confirm whether your corporation has a balance in its Capital Dividend Account (CDA). The CDA accumulates the non-taxable portion of capital gains your corporation has realized, certain life insurance proceeds, and capital dividends received from other private corporations. Whatever sits in the CDA can be paid to you as a capital dividend, which is completely tax-free in your hands.

This is the most consistently overlooked tool for incorporated agency owners. If your corporation has sold equipment, received life insurance, or has been investing retained earnings for several years, there may be a CDA balance available right now. Paying it out requires a board resolution and a special election filed with CRA before the dividend is paid, per the rules under the Income Tax Act administered by the Canada Revenue Agency. It is not complicated, but it absolutely must be done in the right order and with proper documentation.

"The first question in any year-end compensation review is whether there is a Capital Dividend Account balance," says Tara Robertson, CPA, CGA, Senior Tax Accountant at Zenbooks. "That is tax-free money. If it is sitting there and you are paying personal tax on dividends instead, that is an avoidable cost."

Step Two: Check the Refundable Dividend Tax on Hand (RDTOH)

If your corporation has started accumulating passive investment income, either from retained earnings invested inside the company or from a connected holding structure, it may have a balance in its Refundable Dividend Tax on Hand (RDTOH) account. The corporation pays a high refundable tax rate on passive income, but that tax is refunded at a rate of $38.33 for every $100 of taxable dividends paid to shareholders.

This means there are situations where paying a dividend is not just a compensation decision, it is a mechanism to recover corporate tax already paid. The sequencing matters: CDA first, then any RDTOH-triggering dividend payout, then the regular salary and dividend mix.

This level of planning typically becomes relevant once your agency is consistently retaining significant profits and investing them inside the corporation. If you are at that stage, this is a strong argument for having a holding company structure reviewed alongside your operating company compensation plan, which we will come back to.

Step Three: Set a Salary Anchored to Your Real Planning Goals

Once the CDA and RDTOH positions are cleared, the salary question is not primarily a tax question. It is a retirement architecture question.

Salary/bonus/commissions are the only form of compensation that generates RRSP contribution room (18% of earned income, up to $32,490 for 2025)(dividends don’t), builds CPP contributions, enables the lower-income spouse to claim childcare expenses, and supports spousal RRSP contributions. Dividends do none of these things. A T5 generates no RRSP room and no CPP, and the grossed-up dividend income can actually reduce income-tested benefits like the Canada Child Benefit.

The planning consensus is that agency owners who are entirely on dividends are making a 20-year decision with a one-year lens. The tax savings in year one rarely outweigh the compounding cost of arriving at age 55 with no RRSP room, no CPP, and no retirement savings built in a spouse's name.

Our general framework for calibrating salary:

- If CPP in retirement matters to you as a baseline, target salary at least up to the maximum pensionable earnings, which is $71,300 for 2025. That generates combined employer and employee CPP contributions of $8,860 and builds toward a maximum benefit of approximately $1,433 per month at age 65.

- If RRSP contributions are part of your retirement strategy, you need enough salary to generate the contribution room you want to use. To maximize the 2025 RRSP limit of $32,490, you need earned income of approximately $180,500 in the prior year.

- If your spouse has lower income and you want to fund a spousal RRSP, salary is what enables that. Dividends do not.

For most marketing agency owners in the $200K to $500K personal income range, a salary in the $80K to $180K range, calibrated to one of the above targets, is the starting point. Everything above that threshold can be structured as dividends, paid after year-end once the draft financials confirm what the corporation can actually support.

"We see a lot of agency founders who picked a salary number because it matched what they used to earn at an agency job," says Eric Saumure, CPA, CA, Principal, Zenbooks. "That number has nothing to do with their RRSP room or their CPP target. The right number comes from modeling backward from retirement goals, not forward from gut feel."

Step Four: Use Your Agency's Cash Flow Cycle as a Feature, Not a Bug

The feast-or-famine revenue pattern most agencies experience is actually an argument for a fixed, conservative salary, not against one. Set your monthly salary at a number you can sustain even in a slow quarter. This forces personal financial discipline, separates your lifestyle from your billing cycle, and eliminates the temptation to draw cash reactively when the bank account looks full.

Dividends, by contrast, can be declared at any time and do not require a payroll cycle. This makes them the natural vehicle for distributing year-end profit after your accountant has confirmed what is available, what the RDTOH position looks like, and what your RRSP and CPP targets are for the year. The T5 is filed once, at year-end, with a board resolution. No monthly remittances, no monthly payroll deadlines.

The practical structure: a fixed monthly T4 salary to cover personal fixed costs, and a dividend declared in Q1 of the following year once the prior year's numbers are clean. That is not just tax planning. That is the foundation of a cash flow management system that works for a project-based business.

The Sterling Sky case study on our marketing and creative agencies page illustrates what this kind of financial structure enables at scale: a digital marketing consultancy that grew from $1M in revenue in 2018 to over $5M by 2024, with accounting and tax infrastructure that kept pace with that growth.

Step Five: Review Family Member Compensation Through a TOSI Lens

If your spouse, adult children, or other family members are genuinely involved in the agency, even in a part-time or administrative capacity, their compensation deserves a serious review. Many agency founders significantly underestimate or undercompensate family members who contribute real value, and that has a direct tax cost.

Salary paid to a family member who provides legitimate services is deductible to the corporation, provided it is reasonable in relation to the work performed, as required under the Income Tax Act. Many underestimate the value of family help. If a spouse handles client invoicing, contractor coordination, or business administration for 15 hours a week, a salary that reflects that contribution is defensible and reduces corporate taxable income.

The more complex question is whether family members who hold shares in the corporation can receive dividends. The Tax on Split Income (TOSI) rules, which came into effect in 2018, significantly restricted dividend splitting with family members unless specific exemptions apply, including active involvement in the business, age thresholds, and the nature of the income. These rules are not simple, and applying them incorrectly creates CRA risk.

Our practice on this: if a share structure exists or is being considered that could allow dividends to flow to a spouse or adult child, we recommend a written memorandum prepared before any dividends are declared. The memo documents which TOSI exemption applies, the factual basis for that exemption, and how the dividend was determined. That documentation is what protects you if CRA ever asks.

Our Zenbooks tax services team handles exactly this kind of planning memo as part of year-end compensation reviews.

When a Holding Company Becomes Part of the Conversation

A holding company is not a sign that your agency has reached some elite tier of complexity. It is an asset protection and tax deferral tool that becomes relevant when you are consistently generating more profit than you need personally each year.

The mechanism is straightforward: your operating company pays a tax-free intercorporate dividend to a holding company you own. The funds sit inside the HoldCo, protected from creditors of the operating company, and can be invested or distributed strategically over time. The HoldCo also plays a role in preserving the Lifetime Capital Gains Exemption, currently $1,250,000 on the sale of Qualified Small Business Corporation shares, by keeping the operating company's asset mix clean.

One important threshold to track: once passive income inside an associated holding company exceeds $50,000 in a year, your operating company's Small Business Deduction begins to erode, reducing the low ~12% corporate rate on active business income. Your accountant should model this before significant passive investments accumulate.

The Annual Compensation Review: A Process, Not a Conversation

All of this works best when it is treated as a structured annual process rather than a reactive year-end conversation. Here is the framework we run through with agency clients:

Check the Capital Dividend Account balance. Review the RDTOH position. Confirm the prior year's RRSP room used and room available. Model the salary needed to hit this year's RRSP contribution target. Confirm the CPP contribution level and whether the owner wants to continue building toward maximum benefits. Review family member compensation for reasonableness and TOSI compliance. Declare dividends after the draft year-end financials are complete. Document everything with board resolutions and the appropriate T4 and T5 filings.

This is not a complex process. It takes a few hours once a year with the right accounting partner. What it replaces is years of default decisions that quietly cost tens of thousands of dollars in foregone RRSP room, unnecessary tax, and missed tax-free distributions.

Our Technology in Accounting study found that 62% of Canadian business owners handle their own bookkeeping entirely. For an agency owner with genuine financial literacy and a growing business, the compensation planning layer is where the cost of doing it alone is highest and least visible until it is too late to fix.

If you want to know where your agency stands, the Zenbooks Financial Clarity Assessment gives you an immediate picture of your financial management gaps, including whether your compensation structure is costing you money it should not be.

Frequently Asked Questions

Should I pay myself salary or dividends as a marketing agency owner in Canada?

Most agency owners benefit from a hybrid: a fixed monthly salary calibrated to RRSP contribution goals and CPP targets, topped up with dividends declared after year-end once profitability is confirmed. Neither salary alone nor dividends alone is optimal for most founder-operators.

What is the Capital Dividend Account and why does it matter?

The Capital Dividend Account (CDA) accumulates the tax-free portion of capital gains and certain insurance proceeds inside your corporation. Amounts in the CDA can be paid to shareholders as tax-free capital dividends. It should be reviewed before any other compensation decisions are made each year.

What is RDTOH and how does it affect my dividend strategy?

Refundable Dividend Tax on Hand (RDTOH) is a balance that builds when your corporation earns passive investment income. The corporation can recover that tax at a rate of $38.33 per $100 of taxable dividends paid to shareholders. When an RDTOH balance exists, paying a dividend has a dual purpose: personal compensation and corporate tax recovery.

Can I pay dividends to my spouse as a marketing agency owner?

Possibly, depending on your share structure and whether your situation qualifies under a TOSI exemption. The Tax on Split Income rules introduced in 2018 significantly restrict dividend splitting with family members. We recommend a written memorandum documenting the applicable exemption before any family member dividends are declared.

What salary do I need to maximize my RRSP contributions in 2025?

To contribute the maximum $32,490 to your RRSP in 2025, you need earned income of approximately $180,500 in 2024. Dividends do not generate RRSP room, so if RRSP contributions are part of your retirement strategy, salary must be part of your compensation mix.

When does a holding company make sense for an agency owner?

A holding company becomes worth considering when you are consistently generating more profit than you need personally each year and want to protect retained earnings from operating company creditors, preserve LCGE eligibility, or create a more flexible investment and distribution structure. Annual professional fees for a HoldCo typically run $2,500 to $4,000, so the math should justify the cost.

How does agency cash flow affect how I should structure compensation?

Because agency revenue is project-based and irregular, a fixed monthly salary set at a conservative level provides personal financial stability and separates your lifestyle costs from your billing cycle. Dividends can be declared at any time and are best calibrated to year-end profitability rather than monthly cash flow.

Albert Park holds a Master of Taxation from the University of Waterloo and a Bachelor of Commerce from the Rotman Commerce program at the University of Toronto. He is a Chartered Professional Accountant in Canada and a licensed CPA in the State of Illinois. One of a small number of practitioners in Canada to hold both designations. His MTax research focused on GST/HST compliance and administrative design.

Before joining Zenbooks, Albert spent eight years in the tax practice at Ernst & Young (EY), where he advised clients across a range of industries on Canadian and cross-border tax matters. He now serves as Senior Tax Manager at Zenbooks, specializing in Canadian corporate tax, owner-manager tax planning, and Canadian-US cross-border structures for small and mid-sized businesses.

Albert's analysis of Canadian tax policy has been published in Canadian Accountant and Wagepoint.

Subscribe for Updates

Business Clarity That Helps You Breathe Easy

Achieve your business goals and peace of mind with Zenbooks. As both your finance team and business advisor, we empower you every step of the way.