Why Your Bookkeeper Has Never Worked With a Retainer-Based Business Before (And Why That's Killing Your Margins)

Most marketing agency owners who come to us have the same look when we open their books for the first time. It's not embarrassment exactly. It's the look of someone who just realized they've been flying without instruments.

Their revenue is overstated. Their profitability is a guess. Their cash flow projections are built on numbers that don't reflect how the business actually earns money. And in almost every case, it's not because the agency owner doesn't understand their business. It's because their bookkeeper does not.

Bookkeeping for a marketing agency is not the same as bookkeeping for a retail store, a law firm, or a construction company. The revenue structure is fundamentally different. The contractor relationships are more complex. The compliance obligations around HST and T4As carry real risk. And the consequences of getting it wrong don't show up immediately. They show up six months later, when you can't figure out why you're profitable on paper but always short on cash.

This is not a small problem. According to Zenbooks' technology-in-accounting study of 500 Canadian SMEs, managing cash flow is the top business headache for 34% of Canadian SME owners. In our experience, a large share of that pain is not a revenue problem. It's a bookkeeping accuracy problem.

Retainers Are Not Revenue. They Are a Liability Until You Earn Them.

This is where most generalist bookkeepers get agencies into trouble, and they do it from day one.

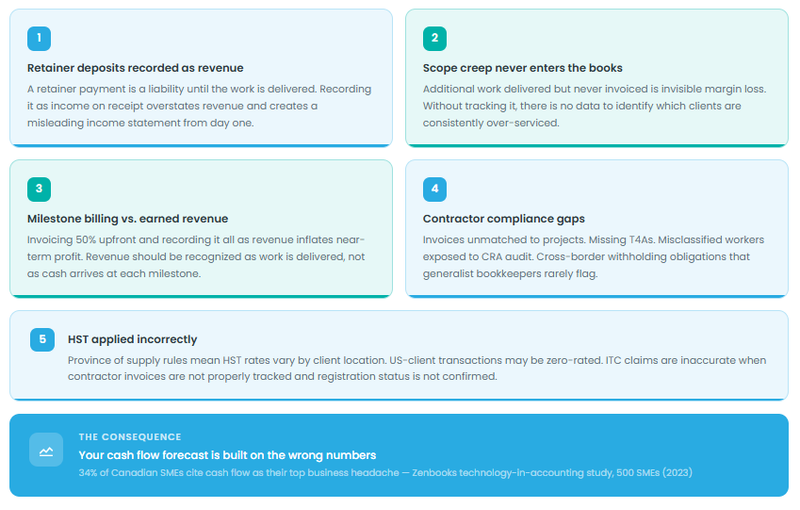

Here is what we see constantly: a client pays a $10,000 monthly retainer on the first of the month. The bookkeeper records it as revenue immediately. It shows up on the income statement. The owner looks at their numbers, sees a profitable month, and makes decisions based on that.

The problem is that $10,000 is not revenue yet. It is a deposit. The agency has not delivered the work. Under Canadian accounting standards, revenue is recognized when it is earned, meaning when the service has been performed. Until then, that money belongs on the balance sheet as deferred revenue, a liability.

When a bookkeeper skips deferred revenue entirely, a few things happen:

- Revenue looks higher than it actually is in the current period

- If a client cancels mid-month, the agency may owe money back, but the books show no obligation

- Next month you may have an enormous amount of deliverables to do while to cash comes in to pay contractors

- The income statement stops being a reliable indicator of business health

- Any financial forecast built on top of those numbers is wrong from the first cell

We onboard new clients regularly whose books have no deferred revenue account at all. This is not a minor technical omission. It is a structural flaw that distorts every financial statement the agency has ever produced.

Scope Creep Is Invisible Revenue, and Most Bookkeepers Never Capture It

Scope creep is the agency industry's most accepted form of leaking margin. A client asks for "one extra round of revisions." A campaign runs three weeks longer than planned. A strategy deck turns into a full brand audit. The account lead says yes, the team does the work, and no one opens a change order.

Scope creep is a business problem. But it is also a bookkeeping problem, because when additional work is performed and never invoiced, it never appears in the books. There is no record that the agency delivered more than the retainer covered. There is no data to show which clients are systemically scope-creeping. There is no way to calculate true project margin.

A bookkeeper who understands agency operations will flag when time tracked against a project significantly exceeds what was budgeted and invoiced. They will work with you to build a process for capturing additional billings. They will make sure that when scope creep happens and gets written off as a business decision, it is a conscious decision, not an invisible one.

Most generalist bookkeepers do none of this. They record what they receive. What is never invoiced simply disappears from the financial picture entirely.

Milestone Billing: The Gap Between Cash and Earned Revenue

Project-based work creates a different but equally significant problem. Many agencies invoice at milestones: 50% upfront, 50% on delivery, or in thirds across a project timeline. On the surface, this is a reasonable billing structure. In the books, it creates a serious matching problem.

Here is the scenario we see regularly: an agency lands a $90,000 brand project. They invoice $45,000 upfront. The bookkeeper records $45,000 in revenue. The agency spends two months building the strategy, creative, and assets. The cash is mostly gone. The project is half done. The income statement says the agency had a strong quarter.

The profitability on that project is actually unknown until delivery is complete and costs are matched against it. Over-invoicing early inflates the income statement in the near term and obscures the true margin of the project. If the project runs over, if the client asks for changes, or if the relationship ends before final delivery, the financial picture can shift dramatically. We all know the last 10% of the work is where all the stress/time is spent. The books won't tell you that. Not if the revenue was recorded at billing rather than at delivery.

Proper bookkeeping matches revenue to the work performed. For milestone-billed projects, that means tracking work in progress, recognizing revenue incrementally as deliverables are completed, and keeping deferred revenue accurate throughout the project lifecycle.

Contractors Are Not Employees. Except When They Are.

Marketing agencies run on contractors. Copywriters, designers, videographers, media buyers, web developers. The flexible labour model is part of what makes agencies scalable. It is also one of the areas where bookkeeping errors carry the most risk.

There are three distinct contractor problems we encounter when onboarding agency clients, and all three require different treatment in the books.

Problem 1: Contractor Invoices Not Tracked Against Project Budgets

The most common issue. An agency pays a contractor $4,000 to build a campaign. The invoice is recorded as an expense. But no one tracks that expense against the specific project it belongs to. The result: no visibility into project-level profitability. You know your total contractor spend. You do not know whether any individual project made money.

This is a job costing problem, and it is fixable with the right bookkeeping structure. Every contractor invoice should be coded to the project it relates to. Without that, your P&L is a summary of what you spent. It is not a management tool.

Problem 2: Misclassified Workers

Canada Revenue Agency has specific criteria for distinguishing an independent contractor from an employee. The distinction is not based on what you call the relationship or what the contract says. It is based on how the work actually functions: who controls the hours, who owns the tools, whether the worker has financial risk, whether they work for other clients.

Agencies frequently have long-term "contractors" who work exclusively for them, take direction on their schedule, use agency-provided software, and operate in every meaningful way as employees. CRA can and does reclassify these workers retroactively. When that happens, the agency owes back CPP contributions, EI premiums, and potentially penalties.

A bookkeeper with agency experience will flag these relationships early. A generalist will record the invoices and move on.

Problem 3: Cross-Border Contractors and T4A Obligations

Canadian agencies increasingly work with contractors in the United States, Europe, and Latin America. This creates two overlapping issues.

First, cross-border payments to non-residents may trigger withholding tax obligations under the Income Tax Act, depending on the nature of the services and the applicable tax treaty. Most generalist bookkeepers are not equipped to identify when this applies.

Second, T4A slips are required for any Canadian resident contractor who was paid $500 or more in a calendar year for services. This is not optional. While the CRA has not really been aggressive in issuing penalties for this, it is a CRA compliance requirement. Missed T4As expose the agency to penalties, and many agencies simply do not know which of their contractors should have received one.

Getting contractor bookkeeping right is not just about clean records. It is about having the right data to issue T4As accurately, identify potential misclassification risk, and avoid surprises in a CRA audit.

HST: Creative Services Are Not All Treated the Same Way

HST on creative and marketing services is more nuanced than most agency owners realize, and generalist bookkeepers often apply a blanket approach that creates problems on both the collection and input tax credit side.

Most services provided by a Canadian marketing agency to a Canadian client are taxable supplies, and HST must be collected. But agencies frequently work with clients across Canada who are in different provinces, which means GST/HST or QST applies at different rates depending on where the client is. This is not complicated for a bookkeeper who understands the rules, but it is a frequent source of under-collection or over-remittance when it is handled incorrectly.

On the expense side, agencies are entitled to claim input tax credits on HST paid on business expenses, including contractor invoices. But if contractor invoices are not being properly tracked, or if invoices from non-GST-registered contractors are being processed without confirming their registration status, the ITC claims can be inaccurate.

The HST issues alone are not a reason to panic. But they are a reason to make sure your bookkeeper understands the service industry, not just the mechanics of double-entry bookkeeping. Are you even charging the right sales tax when selling to a US-based client?...

What This Means for Cash Flow Forecasting

Here is the practical consequence of all of the above: if your books are inaccurate, your cash flow forecast is fiction.

Cash flow forecasting for a marketing agency is already genuinely difficult. You have retainer clients whose contracts might renew or might not. You have project clients whose timelines slip. You have contractor costs that spike when you win a large piece of work. You have milestone invoices that land in one month but fund work spread across three. There are a lot of variables.

All of that complexity is manageable if your books are accurate. Your deferred revenue balance tells you what you have collected but not yet earned. Your work-in-progress tells you what you have earned but not yet invoiced. Your project-coded expenses tell you what margin looks like by client and by engagement. That is the foundation from which a real forecast is built.

Without it, you are forecasting from a bank balance. And a bank balance does not tell you whether the $50,000 sitting in your account is yours or whether it belongs to clients whose work you haven't delivered yet.

Our Zenbooks research on financial technology adoption among Canadian SMEs found that only one-third of SME owners reported being very satisfied with how their accounting and bookkeeping needs were being addressed. For agencies, where the revenue model is inherently more complex than most sectors, that gap between adequate and accurate bookkeeping has real financial consequences.

A Composite Example: What We Actually See at Onboarding

Here is a composite scenario based on the pattern we encounter regularly when onboarding new agency clients.

A digital marketing agency with eight employees and a mix of retainer and project clients approached Zenbooks after their previous bookkeeper moved on. Annual revenue is approximately $1.2 million. The owner believes they are running at around 20% net margin based on their year-end statements.

When we opened the books, here is what we found:

- No deferred revenue account. Retainer payments are being recorded as revenue on receipt, not as earned

- Three long-term contractors who invoice monthly, work exclusively for the agency, and have never had a T4A issued

- Contractor invoices coded to a single "subcontractor" expense account with no project-level allocation

- Two US-based contractors whose payments have never been reviewed for withholding tax obligations

- HST collected at 13% on all invoices regardless of province of supply

After we restate the books with proper deferred revenue treatment and matched project costs, the actual net margin for the prior year is closer to 11%. The agency was not unprofitable. But the owner had been making hiring and pricing decisions based on a number that was nine points too high.

That is the cost of a generalist bookkeeper in a specialist business.

What Proper Agency Bookkeeping Actually Looks Like

Getting this right requires a bookkeeper who understands not just accounting standards but the commercial structure of your business. Specifically:

- Deferred revenue accounts that are updated as retainer work is delivered each month

- Work-in-progress tracking for project-based engagements

- Contractor invoices coded to client projects, not just to an expense category

- Annual T4A compliance review for all Canadian contractors over the $500 threshold

- HST setup that accounts for province of supply and client registration status

- Contractor relationship review to identify potential misclassification risk

None of this is exotic. It is standard accounting practice applied correctly to the agency model. But it requires someone who knows what questions to ask and what to look for when they open your books for the first time.

The Zenbooks research we conducted with 500 Canadian SME owners also found that managing cash flow tied with paying bills as the leading financial pain point. For agencies specifically, accurate bookkeeping is the single most important input to solving that problem. You cannot forecast what you cannot accurately measure.

Reviews From Agency and Professional Services Clients

We work with marketing agencies and professional services firms across Canada. Here is what some of our agency clients have said (full reviews here):

"Zenbooks is the best accounting firm I've ever worked with. I reached out to them with an urgent accounting matter and within 48 hours they solved the problem. They are an innovative and dynamic team who use a number of different technologies and software to deliver financial solutions. I recommend them without hesitation." — Emrah Eren, Duco

"Zenbooks has been an incredible team to work with. They have allowed our design firm to focus on growing and providing a high quality of service to our clients while they take care of the behind the scenes administrative bookkeeping & accounting transactions. Having a bookkeeping company we can trust with great communication and an open mind has provided a tailored service that best suits our needs. As entrepreneurs we invest a lot of time into our craft and require a bookkeeping team that understands our quick pace and constantly evolving needs. They truly take the time to listen and capture our unique requirements and customize their services appropriately. Their team is down to earth and an absolute pleasure to work with. They’re detail oriented and on the ball when it comes to deliverables so that we can analyze the data and make the educated decisions on how to grow our business. We highly recommend Zenbooks and definitely wouldn’t be where we are without them. They’re a key component of our success and our day to day productivity. Thanks for being on our team :)" Justin Thomason, West of Main

Read our full case study of Sterling Sky (SEO Agency) here

Frequently Asked Questions

What is deferred revenue and why does it matter for marketing agencies?

Deferred revenue is money you have collected but not yet earned. For a marketing agency, this typically means retainer payments received at the start of a month before the work has been delivered. Under Canadian accounting standards, revenue is recognized when it is earned, not when cash is received. If your bookkeeper records retainer payments as revenue immediately, your income statement will overstate your earnings and your balance sheet will be missing a liability. This affects every financial decision you make, from hiring to pricing to growth planning.

Do I need to issue T4As to my contractors?

If you paid a Canadian resident contractor $500 or more for services in a calendar year, you are required to issue a T4A slip. This applies regardless of whether the contractor invoiced you as a business or as an individual. T4As must be filed with CRA by the last day of February following the calendar year in which the payments were made. Missing T4As expose you to penalties. Many agencies do not track this correctly because their bookkeeper does not flag it proactively.

How do I know if my contractor should actually be classified as an employee?

CRA looks at a set of factors to determine whether a working relationship is employment or independent contracting: control over how and when the work is done, ownership of tools and equipment, financial risk, and whether the worker is integrated into the business. If a contractor works exclusively for you, follows your schedule, uses your software, and has no real risk of financial loss, CRA may view that as employment. The label on the contract is not determinative. If you have contractors who fit this description, it is worth reviewing the classification before CRA does.

Is bookkeeping for a marketing agency different from other professional services?

Yes, meaningfully so. Marketing agencies combine three revenue structures that most professional services firms do not: recurring retainers, milestone-billed projects, and ad hoc work. Each one requires different revenue recognition treatment. Add to that the contractor-heavy staffing model, the cross-border payment complexity, and the HST considerations around province of supply, and you have a business that genuinely requires a bookkeeper with industry familiarity, not just general accounting competency.

How can better bookkeeping improve my cash flow forecasting?

Cash flow forecasting for an agency is already complex because of the variability in retainer renewals, project timelines, and contractor costs. Accurate books give you the foundation to forecast from real numbers: your deferred revenue tells you what you have collected but not delivered, your work-in-progress tells you what you have delivered but not invoiced, and your project-coded expenses tell you what margin looks like on each engagement. Without that accuracy, you are forecasting from a bank balance, which tells you almost nothing about what is actually yours.

If your marketing agency is scaling and your books have not kept up, the gap between what your financials show and what is actually happening tends to grow, not shrink. Book a free consultation with the Zenbooks team to find out what your books are actually telling you.

Jessica Wong, CPA, CA, leads operations and accounting services at Zenbooks, where she helps growing Canadian businesses get accurate books, practical insights and a better client experience.

Subscribe for Updates

Business Clarity That Helps You Breathe Easy

Achieve your business goals and peace of mind with Zenbooks. As both your finance team and business advisor, we empower you every step of the way.