When to Set Up a Holding Company for Your Marketing Agency

Most marketing agency founders ask about holding companies at the wrong time.

They ask at $4 million in revenue, or after they have already accumulated $300,000 in retained earnings inside their operating company, or, most painfully, the year after they paid a large personal tax bill that proper structuring would have deferred entirely. The question is not wrong. The timing almost always is.

This article is for agency founders approaching the $3M–$5M revenue range who are generating real profit, retaining earnings, and starting to wonder whether their current single-corporation structure is still the right tool for where they are going. The short answer: it almost certainly is not. The longer answer is what follows.

Why a Single Operating Company Starts Working Against You

When you incorporated your agency, you made the right call. A corporation gives you access to the small business tax rate, federally, around 9% on the first $500,000 of active business income, compared to the 46%–53% you would pay personally depending on your province. That gap is real money.

But a single operating company has structural limitations that compound as you grow. Everything lives in one legal box: your client contracts, your intellectual property, your retained earnings, your staff, your brand, and your exposure to any legal, employment, or client dispute. Risk and value sit side by side with no separation between them.

Past a certain threshold, this is not just a legal problem. It is a tax problem. And it is a wealth-building problem.

What a Holding Company Actually Does

A holding company (HoldCo) is a separate corporation that owns shares of your operating company (OpCo). It does not run a business. It holds wealth: investments, real estate, accumulated earnings, and in many cases the shares of the OpCo itself.

The core mechanism is straightforward. Your OpCo earns active business income, pays corporate tax on it, and then pays the after-tax surplus upward to the HoldCo as an inter-company dividend. Under Section 112 of the Income Tax Act, that dividend is received by the HoldCo tax-free. As long as the share structure is set up correctly, moving it between related corporations does not trigger a second tax event.

What this means in practice: you can accumulate and invest significant capital inside a HoldCo without the funds being subject to personal income tax until you actually withdraw them. You control the timing of that withdrawal. That control is worth a great deal.

The HoldCo also creates legal separation. Creditors of the OpCo generally cannot reach assets held in the HoldCo. If your agency ever faces a large client claim, a payroll dispute, or an employment lawsuit, the funds you have moved to the HoldCo are protected.

One important caveat: this article addresses holding company structure for wealth protection and tax deferral during the growth phase of your agency. If a future sale and the Lifetime Capital Gains Exemption (LCGE) are part of your planning horizon, the structure needs additional analysis, a HoldCo owning OpCo shares without proper planning can affect your eligibility for the LCGE exemption on a qualifying sale. A trust in between can solve this, but worth noting here.

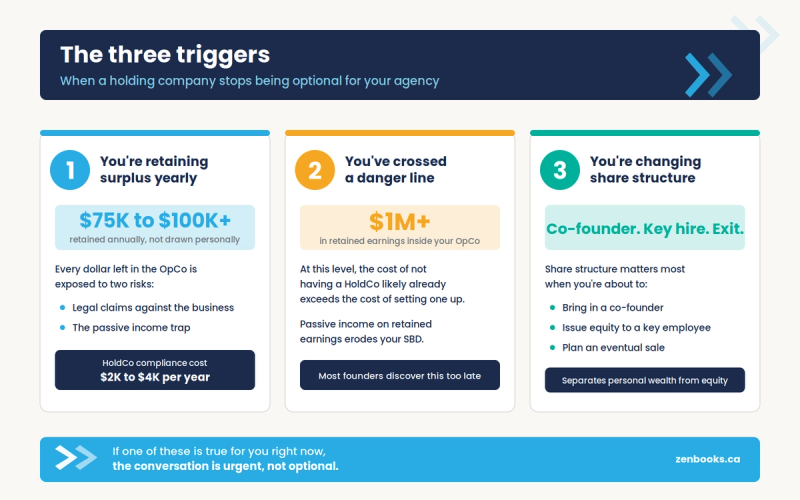

The Three Triggers: When the Math Flips in Your Favour

There is no single right answer on timing, but there are three conditions that, when present, make the conversation urgent rather than optional.

Trigger 1: You are retaining more than $75,000–$100,000 annually and not spending it personally.

If your agency generates, say, $500,000 in pre-tax active business income and you are living on $150,000–$200,000, you are accumulating meaningful surplus every year. Every dollar of that surplus that sits in the OpCo is exposed to the passive income trap (more on this below) and unprotected from legal risk. Moving it to a HoldCo costs very little in annual compliance fees relative to what it protects.

Trigger 2: You have crossed $1M in retained earnings inside your operating company.

At this point, the cost of not having a HoldCo has likely already exceeded the cost of setting one up. You also begin to approach territory where the passive income earned on those retained earnings starts to affect your small business deduction, a consequence most agency founders discover after the fact.

Trigger 3: You are thinking about bringing in a co-founder, issuing shares to a key employee, or planning for an eventual sale.

Share structure matters enormously in these scenarios. A HoldCo creates a cleaner separation of personal wealth from business equity and makes it easier to issue equity in the OpCo without encumbering your personal accumulated assets.

We also have a HoldCo analyser in which you can answer 9 questions and get a structured, honest assessment of whether a Holdco makes sense for your situation, including the trade-offs to discuss with your advisors.

HoldCo Analyser

The $50,000 Passive Income Trap Most Agency Owners Don't Know About

This is arguably the most consequential piece of tax mechanics that agency founders at this stage have never heard of.

The small business deduction (SBD) allows your CCPC to pay the reduced 9% federal corporate tax rate on up to $500,000 of active business income. Most founders know this. What most founders do not know is that the SBD begins to be clawed back once your corporation earns more than $50,000 in passive investment income in a year.

The clawback is steep: for every $1 of passive income above $50,000, your SBD business limit is reduced by $5. The SBD is fully eliminated at $150,000 in passive income. At that point, your active business income is taxed at the general corporate rate of approximately 27%.

If you have $1.5M sitting in your OpCo invested in a diversified portfolio earning a conservative 5% return, you are generating $75,000 in passive income and your SBD is already reduced by $125,000. That is not a theoretical problem. It is a real, recurring annual tax cost.

Moving accumulated earnings to a HoldCo via a Section 112 inter-company dividend provides legal protection and estate planning benefits, but it does not solve the passive income SBD problem on its own. Because a HoldCo and OpCo are almost always associated corporations under ITA S.125(5.1), the AAII formula includes passive income earned across all associated corporations. The HoldCo's investment income counts against the OpCo's SBD just as if it were sitting in the OpCo itself.

The real levers for SBD preservation are investment mix management (favouring growth assets over income-producing ones to minimize annual AAII), Series T mutual funds that distribute primarily return of capital, and careful timing of capital gains realization. These strategies your advisor should be modelling annually.

This is one of the most concrete, quantifiable reasons to act on HoldCo structuring before you need it.

What This Looks Like in Practice: Two Client Scenarios

Client A is a branding and digital agency in Ontario with approximately $3.2M in revenue and a net margin of around 22% after owner salary. Over five years of operating as a single corporation, they had accumulated roughly $680,000 in retained earnings, all sitting in the OpCo. We modelled the passive income exposure: at their current investment return, they were on track to cross the $50,000 passive income threshold within 18 months. We established a HoldCo, restructured the share ownership so the HoldCo held the OpCo shares, and began paying inter-company dividends annually. Within two years, the combined structure provided full legal protection of the accumulated capital and a clear investment strategy designed to minimize AAII across both corporations, with annual CPA review to keep passive income below the $50,000 threshold.

Client B is a performance marketing agency with two founders, both in their late thirties, with a combined household income that placed them consistently at the top marginal rate. They had been paying themselves primarily in salary because their accountant had not discussed dividend planning at the corporate level. When they came to Zenbooks, we restructured the ownership so that the HoldCo held the OpCo shares, established a separate class of shares for each founder's HoldCo, and put a dividend policy in place that allowed for flexible annual distributions based on each founder's personal income for that year. In the first full tax year under the new structure, the combined personal tax deferral was approximately $47,000.

Both of these outcomes required CPA-level tax planning. Neither was complex once the structure was in place. Both were entirely unavailable inside a single operating company.

It's worth noting that this structure was implemented with the founders' medium-term goals in mind, not as a pre-sale structure. Founders who anticipate a sale and want to preserve LCGE eligibility need a separate, specific analysis before restructuring share ownership.

Profit Sharing: Two Structures, Very Different Tax Outcomes

"Profit sharing" means two different things for agency founders, and the tax treatment of each is different enough that conflating them is a planning error.

Owner-level profit sharing: distributing profits between co-founders, spouses, or family members through dividends, is where TOSI planning (Tax on Split Income) becomes directly relevant. We address this in the next section.

Employee-level profit sharing: formal programs that distribute a percentage of operating profit to your team, is a different conversation. These are generally structured as salary or bonus, which means they are fully deductible to the corporation and fully taxable to the employee. There is no tax magic here, but there is a legitimate retention and performance argument. The caution we offer at Zenbooks is this: agencies below $5M in revenue with variable margins should think carefully before creating formal, contractual profit-sharing obligations with staff. The reputational and morale cost of a year in which you cannot fund the program can exceed the benefit of the years you do. Discretionary bonuses tied to published criteria but not legally obligated tend to perform better at this stage.

TOSI, Income Splitting, and What Your Accountant May Be Getting Wrong

The Tax on Split Income rules, which were significantly expanded in 2018, are widely misunderstood, and that misunderstanding goes in both directions.

Some founders assume that because TOSI exists, income splitting with a spouse is simply off the table. That is not accurate. There are legitimate, CRA-recognized pathways to pay dividends to a spouse or adult family member without triggering TOSI, and agency owners specifically have more options than most service businesses.

The two most relevant exceptions for agency founders are:

The Excluded Business Exception. If your spouse has worked an average of at least 20 hours per week in your agency, either in the current year, or in any five previous taxation years, dividends paid to them are excluded from TOSI entirely, now and in the future. This is not a subjective standard. It requires documentation: time sheets, task records, email chains. Founders whose spouses contribute meaningfully to the business (client management, admin, bookkeeping, marketing, business development) often meet this threshold without knowing it. The planning cost is documentation, not restructuring.

The Excluded Shares Exception. This is the more technical pathway, and the one most accountants either overlook or dismiss without analysis. Under the excluded shares rules, a family member aged 25 or older who directly owns at least 10% of the votes and value of the corporation may receive dividends outside of TOSI, provided the corporation is not a professional corporation, and provided less than 90% of the corporation's gross business income in the prior year came from the provision of services.

That last condition is the critical one for marketing agencies, and it deserves a careful read. If your agency derives even a meaningful portion of its revenue from product sales, licensed software, physical deliverables, media buys billed at markup, or any non-service revenue stream, you may be closer to meeting the 90% threshold test than you think. The analysis is fact-specific and must be done by a CPA, but dismissing it without analysis is leaving real planning on the table.

"The excluded shares exception gets ignored because it takes work to evaluate," says Albert Park, CPA, CA, CPA (IL), MTax, Senior Tax Manager at Zenbooks. "But for an agency with any product or resale revenue, it is worth doing that work. The potential upside, ongoing dividend income to a spouse at a significantly lower marginal rate, can be worth tens of thousands of dollars annually over a planning horizon."

The Capital Dividend Account: The Most Underused Tool in Your Structure

If you have never heard of the Capital Dividend Account (CDA), that is not your fault. It only becomes relevant in specific circumstances. But when it does, it matters enormously.

The CDA is a notional account maintained inside a CCPC. Certain tax-free amounts accumulate in it over time: the non-taxable portion of capital gains (currently 50% of a capital gain is included in income; the other 50% flows to the CDA), life insurance proceeds received by the corporation in excess of the policy's adjusted cost basis, and certain other amounts.

Once funds are in the CDA, they can be paid out to shareholders as a capital dividend, completely tax-free to the recipient.

For an agency founder who carries a corporate-owned life insurance policy (a common and legitimate planning tool), the death benefit above the adjusted cost basis flows entirely into the CDA and can be paid out tax-free to the estate. For founders who eventually sell assets held inside the corporation, the non-taxable portion of the capital gain accumulates in the CDA and can be distributed to shareholders without personal tax.

A properly structured HoldCo does not just protect and grow your wealth. It also positions you to extract that wealth as efficiently as possible when the time comes.

The Salary vs. Dividends Question Is Mostly a Distraction

Agency founders at this stage spend a disproportionate amount of time debating the salary-versus-dividends mix. If that’s you, you can use our Salary vs Dividend tool here. The question is real, the optimal compensation blend does reduce your annual tax burden, but it is not where the structural leverage lives.

The real leverage is in whether retained earnings are protected from personal tax drag at all. The decision about whether to pay yourself $180,000 in salary or $180,000 in dividends is worth a few thousand dollars at the margin. The decision about whether to accumulate $500,000 in a protected HoldCo structure or leave it exposed in your OpCo is worth significantly more, compounded over a decade.

Our research of 500 Canadian SMEs found that 34% of business owners cited cash flow management as their top financial headache, yet only a fraction were receiving proactive planning on how retained earnings could be deployed more strategically. Compensation mix is one part of that. Corporate structure is the bigger part.

That said, the salary-versus-dividends decision does interact with your HoldCo structure in one important way: salary paid by the OpCo creates RRSP contribution room, which a pure dividend strategy does not. For agency founders who want to maximize registered savings alongside their HoldCo accumulation, a blended approach, typically a salary in the range of $175,000–$200,000 to maximize RRSP contributions plus CPP entitlements, with the balance paid as inter-company dividends to the HoldCo, tends to perform well.

What Clients Are Saying

Emrah Eren, founder of Duco, a Zenbooks client in the creative and digital space, described the shift this way: "Zenbooks is the best accounting firm I've ever worked with. I reached out to them with an urgent accounting matter and within 48 hours they solved the problem. They are an innovative and dynamic team who use a number of different technologies and software to deliver financial solutions. I recommend them without hesitation. "

Jake Naylor, founder of Whiskey Jack Media, put it more directly: "signed with them for my company, Whiskeyjack Media, a few months ago. I would describe my feelings as "bananas happy" so far. Wishing I would have called them sooner... Keep up the great work, guys! "

These experiences align with what we see across our portfolio. According to our Technology in Accounting study of 500 Canadian SMEs, only 9% of business owners reported receiving cash flow forecasting services from their accountant. Structural planning, the kind that includes HoldCo strategy, TOSI analysis, and SBD preservation, is even less commonly delivered proactively.

The Compliance Cost Objection

The most common pushback we hear from agency founders who are close to ready is about compliance cost. Running two corporations means two annual corporate tax filings, two sets of financial statements, and somewhat more complex bookkeeping. For most agencies at this revenue level, the incremental annual cost runs between $2,000 and $4,000.

At the margin levels we typically see in well-run marketing agencies, the tax deferral and SBD preservation benefits of a HoldCo structure will exceed that compliance cost within the first year in almost every case. The question is not whether the structure pays for itself. It is whether your current accountant has run those numbers for you. If they have not done so proactively, that silence is costing you something.

A Note on Professional Services vs. Marketing Agencies

One clarification worth making explicitly: the excluded shares exception and several other TOSI planning strategies are not available to professional corporations, defined under the Income Tax Act as corporations carrying on the professional practice of an accountant, dentist, lawyer, medical doctor, veterinarian, or chiropractor.

Marketing, creative, and digital agencies are not professional corporations under this definition. That is not a loophole. It is the intended operation of the rules. Agency founders have access to a broader set of structural planning tools than, say, a dental practice or a law firm. That distinction matters and is worth understanding.

What to Do If You Recognize Your Situation in This Article

The first step is not to incorporate a holding company. The first step is an honest diagnostic of where you are: how much you are retaining annually, what your passive income exposure looks like, whether your spouse contributes to the business, and what your medium-term plans are for the agency.

That diagnostic should be done with a CPA who does this kind of planning regularly, not a compliance-only accountant who files your returns and waits for you to ask questions.

We also have a HoldCo analyser in which you can answer 9 questions and get a structured, honest assessment of whether a Holdco makes sense for your situation, including the trade-offs to discuss with your advisors.

HoldCo Analyser {BUTTON}

If you are a marketing or creative agency founder in the $1M–$10M revenue range, the Zenbooks Financial Clarity Assessment is a useful starting point. It takes about two minutes, gives you an immediate read on where your financial structure stands, and surfaces the specific planning gaps most relevant to your situation.

You can also learn more about how we work with marketing and creative agencies specifically on our agency accounting services page.

The right time to have had this conversation was probably a year ago. The second-best time is now.

Frequently Asked Questions

How much does it cost to set up a holding company in Canada?

The legal cost of incorporating a new HoldCo typically runs between $1,500 and $3,000, depending on your province and the complexity of the share structure. Annual compliance (two corporate tax filings, financial statements) typically adds $2,000–$4,000 per year on top of your existing accounting fees. For most agency founders retaining $100,000 or more annually, this may be recovered through tax deferral and SBD preservation within the first year.

Can I set up a holding company if my agency is already incorporated?

Yes. The most common approach is to incorporate a new HoldCo and then restructure the share ownership of the existing OpCo using a Section 86 share exchange or similar mechanism, which can often be done on a tax-deferred basis. This is not a simple DIY filing, it requires a CPA and usually a corporate lawyer, but it is entirely routine at this stage of business.

Does a holding company protect me from CRA audits?

A holding company does not reduce audit risk, but it does create cleaner separation between your operating activity and your accumulated wealth, which can simplify the audit process. The more important protection is that assets in the HoldCo are not exposed to claims against the OpCo.

Can I pay dividends to my spouse if I have a holding company?

Possibly, depending on your specific circumstances, the structure of the HoldCo, and whether the excluded business or excluded shares exception to TOSI applies. This is a fact-specific analysis that requires professional review before any dividends are declared. The answer is often yes, but the path to getting there requires documentation and proper share structure.

What is the difference between the small business deduction and the general corporate tax rate?

The federal small business deduction reduces the corporate tax rate on the first $500,000 of active business income. Combined with provincial corporate tax, the difference between paying the SBD rate and the general rate on, say, $400,000 of active income can represent a tax cost of $30,000–$50,000 annually, depending on your province.

When should I talk to a CPA about holding company structure?

Proactively, not reactively. The ideal time is when your agency begins retaining meaningful profit beyond your personal draw, or at minimum before you accumulate $500,000 in your operating company. If your current accountant has not raised this topic with you, that is worth noting.

Albert Park holds a Master of Taxation from the University of Waterloo and a Bachelor of Commerce from the Rotman Commerce program at the University of Toronto. He is a Chartered Professional Accountant in Canada and a licensed CPA in the State of Illinois. One of a small number of practitioners in Canada to hold both designations. His MTax research focused on GST/HST compliance and administrative design.

Before joining Zenbooks, Albert spent eight years in the tax practice at Ernst & Young (EY), where he advised clients across a range of industries on Canadian and cross-border tax matters. He now serves as Senior Tax Manager at Zenbooks, specializing in Canadian corporate tax, owner-manager tax planning, and Canadian-US cross-border structures for small and mid-sized businesses.

Albert's analysis of Canadian tax policy has been published in Canadian Accountant and Wagepoint.

Subscribe for Updates

Business Clarity That Helps You Breathe Easy

Achieve your business goals and peace of mind with Zenbooks. As both your finance team and business advisor, we empower you every step of the way.