GST/HST for Canadian Small Business: The $30,000 Threshold, the Quick Method, and What the CRA Actually Wants

The most common GST/HST question I get from new business owners is the wrong question.

It is almost always some version of "do I need to register yet?" The right question, in nine cases out of ten, is "should I register now even though I don't have to?" That distinction sounds small. It is worth thousands of dollars over the first few years of a Canadian business, and almost no one running a new corporation or sole proprietorship is told the difference.

This post is for owners who are at or approaching the start of their GST/HST journey. Pre-registration sole proprietors, brand-new corporations, businesses that crossed the threshold last quarter and now need to figure out what to actually do. By the end you will know what the threshold actually means, when registering early is the smart play, why the Quick Method is good for some businesses and bad for most, how to use your filing frequency as a cash flow tool, and where the federal system stops and the provincial systems begin.

A short note on intellectual honesty before we start. The $30,000 small supplier threshold is the central rule we are about to discuss, and I want to be transparent that I think the rule itself is broken. My colleague Albert Park, CPA, CA, CPA (IL), MTax and I argued in Canadian Accountant in February 2026 that the threshold has not been adjusted once since 1991, that decades of inaction have eroded its real value, and that it now pulls micro-enterprises into mandatory compliance long before they are operationally ready. The rule is what it is until Parliament changes it. But you should know going in that you are complying with a number set during the first Bush US administration.

What the $30,000 Small Supplier Threshold Actually Means

You become legally required to register for GST/HST when your total worldwide taxable revenue (and that of any associated businesses) exceeds $30,000 in a single calendar quarter, or over four consecutive calendar quarters. The rule is set out in the CRA's official guidance on when to register and start charging GST/HST.

Three things about this rule are routinely misunderstood.

It is gross revenue, not profit. A consultant who bills $35,000 in a year and has $20,000 in expenses has crossed the threshold. The $30,000 number ignores your costs entirely.

It is over a rolling four quarters, not a calendar year. If you are at $25,000 in revenue at the end of Q3 and you bill $8,000 in October, you have crossed the threshold. You do not get to wait until December 31 to assess.

Crossing it triggers a hard deadline. Once you cross $30,000 in a single calendar quarter, you must register within 29 days of your first sale that took you over the threshold, and you must charge GST/HST on the sale that put you over. If you cross it gradually over four quarters, your effective registration date is the first day of the second month after the quarter that pushed you over. The detailed rules are in CRA Guide RC4022, General Information for GST/HST Registrants.

The most expensive version of getting this wrong is not the registration itself. It is finding out two years after the fact that you should have been collecting tax the whole time. The CRA can assess you for the GST/HST you should have collected, and you usually cannot retroactively bill the customer for it. That tax comes out of your own pocket, with interest.

If you have already crossed the threshold and not registered, do not wait for the CRA to find you. The Voluntary Disclosures Program can eliminate penalties and reduce interest, but it is only available before the CRA contacts you about the issue.

Why You Should Probably Register Voluntarily Before You Have To

This is the conversation I wish more accountants were having with their new business clients. If your customers are themselves GST/HST registrants, which is true for almost every B2B business in Canada, voluntary registration before the threshold is usually the right call.

Here is the math. When you charge GST/HST to a registered business customer, it costs them nothing. They claim it back as an input tax credit (ITC) on their own return. Meanwhile, you get to claim ITCs on every taxable input you buy: software subscriptions, professional services, office equipment, contractor invoices, the laptop you bought last month. For a typical B2B services business spending $20,000 a year on taxable Canadian inputs, voluntary registration recovers around $2,600 in ITCs annually that would otherwise be a sunk cost.

The trade-off is real but small. You take on the administrative work of charging, tracking, and remitting GST/HST, and you have to file returns even if you have nothing to remit. For a business already using cloud accounting software, that work is largely automated. The Zenbooks Technology in Accounting study, conducted with Abacus Data across 500 Canadian SMEs, found that 68% of Canadian SMEs now have bookkeeping, accounting, and payroll that are mostly or entirely digital. If you are in that 68%, the additional friction of voluntary registration is genuinely minor.

When does voluntary registration not make sense? Two situations. If your customers are individual consumers (B2C) who pay out of pocket and would notice the price increase, you are effectively choosing between absorbing the tax yourself or losing competitive ground. And if your business has almost no taxable inputs (a solo professional working from a home office with minimal expenses), the ITCs you can claim are too small to justify the administrative work.

For everyone else (and that is most growing Canadian businesses) the question is not whether to register voluntarily. It is when. My answer is usually: at incorporation, or as soon as you have a clear path to crossing the threshold.

The corollary to this is something I see often enough to flag: owners who deliberately decline work to stay under $30,000. This is rational only if you sell to consumers and cannot pass the tax through. If you serve B2B customers, the threshold is not a strategic ceiling. Staying small to avoid GST/HST is the tax equivalent of refusing a promotion because you do not want to pay more tax on the higher salary.

How to Register

As of November 3, 2025, the CRA has eliminated phone registration for Business Numbers and program accounts. Registration is now online-only through Business Registration Online (BRO), with mail registration via Form RC1 still available for cases the online portal cannot handle.

The process itself is straightforward.

If you are not yet incorporated and do not have a Business Number, BRO will issue your BN and your GST/HST account (the RT0001 program account) in the same session.

If you incorporated federally or provincially, you almost certainly already have a Business Number and an RC corporate income tax program account. You need to add the RT GST/HST program account to your existing BN through My Business Account.

Either way, you will need: your legal business name, your business address, a description of your business activity, your fiscal year-end, and your estimated annual revenue. Online registrations typically process within a few business days.

A subtle but important choice you make at registration is your effective date. If you are registering voluntarily as a small supplier, your effective date is usually the date of your request, but it can be backdated up to 30 days. Backdating lets you claim ITCs on purchases made in that window. If you have meaningful pre-registration capital expenses, this is worth doing.

Registering for the GST/HST account is just one program account attached to your BN. The same Business Number will also carry your RP payroll account when you hire your first employee, and your RC corporate tax account if you are incorporated.

The Quick Method: A Trap for Most Service Businesses, a Quiet Win for a Specific Subset

The Quick Method of Accounting is a CRA election that lets you remit a flat percentage of your gross taxable sales (including the GST/HST you collected) instead of tracking input tax credits. CRA's marketing of this option is generous and the framing is consistent: "simpler bookkeeping, often a tax saving." This framing is half right.

Here is what is true. The Quick Method genuinely is simpler. You still charge GST/HST normally, but instead of subtracting your ITCs from your collected tax, you remit a flat rate (for example, 8.8% of HST-included revenue for an Ontario service business) and keep the difference. You also get a one-time-per-year 1% credit on your first $30,000 of eligible supplies.

Here is what is not true. The Quick Method is not universally beneficial, and the framing of "you keep the difference" obscures what you are giving up. Under the Quick Method, you forfeit your ITCs on operating expenses entirely. You retain ITCs only on capital purchases of $10,000 or more (vehicles, large equipment, real property).

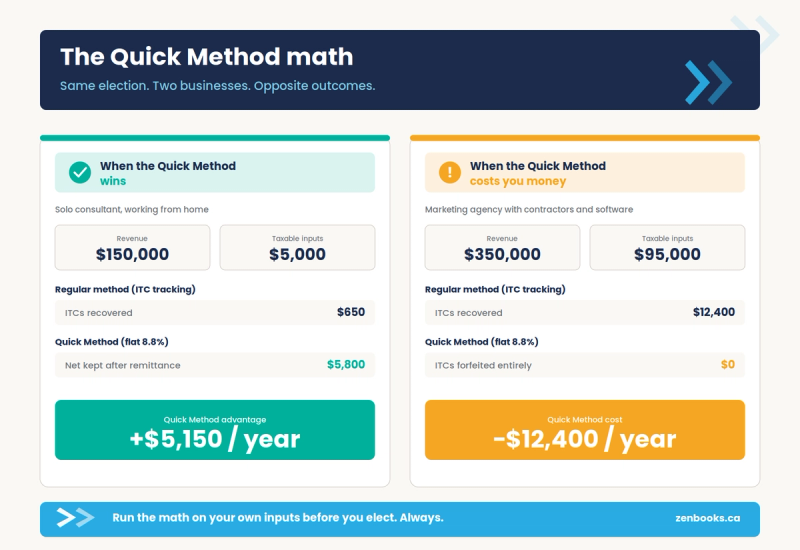

The math works for one specific kind of business: a low-cost service business with very few taxable Canadian inputs. Think a solo consultant working from home, billing $150,000 a year, with maybe $5,000 in software, equipment, and professional services as their entire taxable expense base. Under the regular method they recover $650 in ITCs. Under the Quick Method (8.8% remittance rate, 1% credit on first $30,000), they keep approximately $5,800 of the HST collected. The Quick Method wins by about $5,000.

Now consider a marketing agency with $350,000 in revenue, $80,000 in taxable contractor and software spend, $15,000 in office costs and supplies. ITCs under the regular method are around $12,400. Under the Quick Method, they remit roughly the same amount net, but lose every dollar of ITC on operating expenses. The Quick Method costs them money.

The Quick Method has a hard $400,000 revenue ceiling (you cannot use it if your worldwide taxable revenue exceeded $400,000 in any of the last four consecutive quarters), and several types of businesses are explicitly excluded. Notably, accountants, bookkeepers, lawyers, and financial consultants cannot use the Quick Method. CRA has a specific rule about this.

My strong opinion: the Quick Method is worth modeling for any service business under $400,000 with low taxable input costs. For everyone else, it is a quiet way to leave money on the table. If your accountant has recommended the Quick Method without modeling both methods against your actual expense profile, you should ask them to show you the math.

If you elect into it, you must use the Quick Method for at least one full year before revoking. The election is made on Form GST74, with timing rules that depend on your filing frequency. Annual filers have until the first day of their second fiscal quarter; monthly and quarterly filers must elect by the due date of the return for the period in which they want the method to apply.

Filing Frequency Is a Cash Flow Decision

Once you are registered, the CRA assigns you a default filing frequency based on your total annual taxable revenue. The thresholds, set out in CRA Guide RC4022, are:

- Annual filing: revenue under $1.5 million

- Quarterly filing: revenue between $1.5 million and $6 million

- Monthly filing: revenue over $6 million

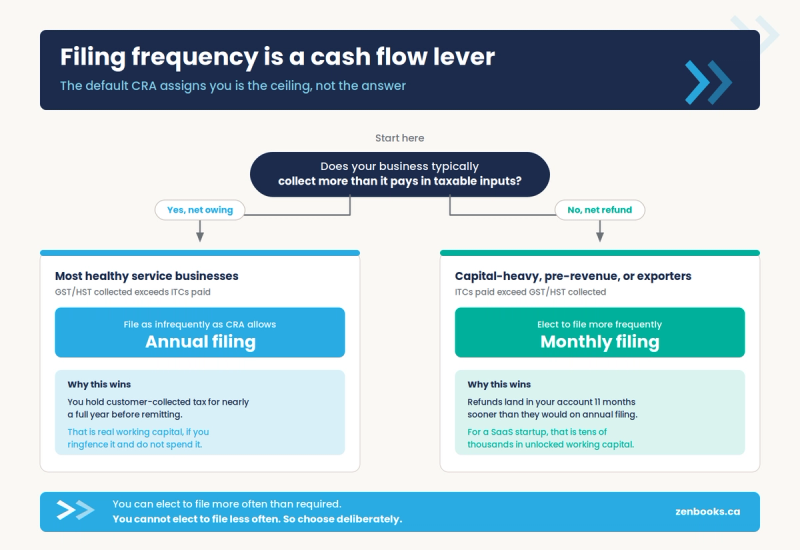

Most owners treat this assignment as a fact of nature. It is not. These thresholds are the maximum frequencies CRA imposes on you based on your size. You can always elect to file more frequently than required. You cannot elect to file less frequently.

This is a cash flow lever that almost nobody talks about, and it matters in both directions.

If your business consistently has GST/HST refundable (you pay more in ITCs than you collect, common for capital-intensive startups, exporters of zero-rated goods, and businesses in heavy growth investment phases) filing monthly instead of annually means you collect your refund 11 months earlier. For a SaaS startup spending heavily on infrastructure, that can be tens of thousands of dollars in working capital that is otherwise locked up at the CRA.

If your business consistently owes GST/HST (you collect more than you spend on taxable inputs, which is most healthy service businesses), staying on annual filing means you hold the cash for nearly a full year before remitting. As long as you discipline yourself to ringfence the collected amount, that is real working capital.

"The single most underused planning lever for businesses approaching the $1.5 million revenue mark is filing frequency," says Albert Park, CPA, CA, CPA (IL), MTax, Senior Tax Manager at Zenbooks. "By the time CRA bumps you to quarterly filing automatically, you have already lost the optionality. Owners should be evaluating whether the default frequency matches their cash position every year, not waiting for the threshold to force the decision."

To change your filing frequency, you file Form GST20, Election for GST/HST Reporting Period, with the CRA. The election generally takes effect at the start of the next fiscal year. Or just do it online in My Business Account.

Mandatory Electronic Filing

For GST/HST reporting periods beginning on or after January 1, 2024, electronic filing is mandatory for all registrants other than selected listed financial institutions and charities. The previous $1.5 million revenue threshold for mandatory e-filing has been removed. Penalties apply for paper filing.

Separately, any payment to the CRA of $10,000 or more must now be made electronically. Cheques are still accepted for smaller amounts but the trajectory is clear: paper is on its way out across the entire compliance system.

If you are still mailing your GST34 return, you are not just creating risk of late processing. You are running a small but real penalty exposure on every filing.

Where Federal Stops and Provincial Begins

The GST/HST is federal. The CRA administers it nationally and the same registration covers your obligations everywhere in Canada that uses HST or GST.

Some provinces stop there. Alberta, the territories, and most of Atlantic Canada (which uses HST through the federal system) have no separate provincial sales tax to register for.

Other provinces run their own parallel sales tax systems, and these require separate registration with the provincial authority.

- Quebec: QST is administered by Revenu Québec and requires a separate NEQ business number and QST registration.

- British Columbia: PST is administered by the BC government with its own registration process.

- Saskatchewan and Manitoba: each runs its own PST regime requiring separate registration.

If you sell into multiple provinces, you may have GST/HST obligations federally and PST or QST obligations provincially, all running in parallel. This is one of the fastest ways for a growing business to fall out of compliance unintentionally. A future post will cover the provincial sales tax landscape in detail.

Case Study: How Kehops Got GST/QST Right During a Co-Founder Exit

Kehops is a Canadian reverse-sourcing platform for corporate team-building. When founder Philippe Boivin came to Zenbooks in late 2024, the company was in the middle of a co-founder separation, the books had not been touched in months, and the previous accountant had filed on the company's behalf without ever giving Philippe direct access to his own CRA My Business Account or Revenu Québec account.

The GST/QST piece was small relative to the broader cleanup, but it illustrates the point. As a Quebec-incorporated business with Stripe revenue, Kehops had simultaneous federal GST and provincial QST obligations to manage, with revenue recognition complexities specific to subscription billing. The previous accountant had handled filings without explaining the underlying mechanics, which meant Philippe had no way to verify whether the filings were accurate or to make informed decisions about timing, frequency, or registration scope.

We restored full access for Philippe to both CRA and Revenu Québec, took over GST/QST filing with proper Stripe revenue recognition, and built the infrastructure to handle ongoing compliance through the convertible note conversion and co-founder buyout. By February 2026, two years of corporate tax returns and GST/QST filings were complete, the books were clean, and the company entered its next funding window with auditable financials.

"When I brought Zenbooks on board, my board needed more than competent accounting," Philippe said. "...gave my board the confidence they needed to approve the engagement unanimously." Read the full Kehops case study for the complete picture.

What a Properly-Run GST/HST Function Looks Like

For most growing Canadian businesses, GST/HST done well looks like this:

Registration is proactive, not reactive. You registered when the math made sense for your business model, not when the CRA forced you to.

Filing frequency is reviewed annually. You do not just accept the default. You assess whether your cash position favours filing more frequently for refunds or annually for cash retention.

Quick Method versus regular method has been modeled at least once. You know which one works for you and you have the spreadsheet to prove it.

Collected GST/HST is segregated. The cash you collect from customers as tax is not your operating cash. It belongs to the federal government and you are holding it in trust.

Year-end ties out to the books. Your GST/HST account in your accounting software reconciles to your filings without surprises.

"What we see most often with new clients is not that they have done anything wrong on GST/HST," says Jessica Wong, CPA, CA, Director of Operations at Zenbooks. "It is that they have never had the conversation about whether the structure they ended up with is the structure they should have chosen. There is a difference between filing accurately and filing strategically, and most owners only get the first one."

The Zenbooks Technology in Accounting study found that only 32% of Canadian SMEs report being "very satisfied" with how their accounting and bookkeeping are handled, and that 1 in 3 feel they have outgrown their current accountant. GST/HST strategy is one of the specific places where that gap shows up. You can read the complete study findings here.

Frequently Asked Questions

What is the GST/HST small supplier threshold in Canada?

The threshold is $30,000 in worldwide taxable revenue (including those of associated businesses) over four consecutive calendar quarters, or in any single calendar quarter. Once you cross it, you must register and begin charging GST/HST. The threshold is set out in CRA's Excise Tax Act guidance on small suppliers.

When do I need to register for GST/HST?

You must register within 29 days of the sale that took you over the $30,000 threshold in a single quarter, or by the first day of the second month after the quarter in which you crossed the threshold gradually. You can also register voluntarily at any time before reaching the threshold.

What is the Quick Method election and should I use it?

The Quick Method lets eligible businesses with under $400,000 in annual revenue remit a flat percentage of GST/HST-included sales instead of tracking input tax credits. It is beneficial for low-cost service businesses with minimal taxable expenses, and harmful for businesses with significant taxable input costs. Accountants, bookkeepers, lawyers, and financial consultants cannot use the Quick Method.

How do I register for a GST/HST account?

As of November 2025, registration is online-only through CRA's Business Registration Online (BRO). You will need your legal business name, address, business activity description, fiscal year-end, and estimated revenue.

How often do I need to file GST/HST returns?

CRA assigns a default frequency based on your annual revenue: annual under $1.5 million, quarterly $1.5 million to $6 million, monthly above $6 million. You can elect to file more frequently than the default, which is useful if you regularly receive refunds.

Can I register for GST/HST before I reach $30,000 in revenue?

Yes. Voluntary registration is permitted at any time and is often the right choice for B2B businesses, because charging GST/HST to registered customers costs them nothing while letting you claim input tax credits on your own taxable purchases.

What happens if I do not register when I should have?

You owe the GST/HST you should have collected from the date you crossed the threshold, with interest and potentially penalties. The Voluntary Disclosures Program can reduce these consequences if you come forward before the CRA contacts you.

Do I need to register separately for QST or PST?

If you have customers in Quebec, BC, Saskatchewan, or Manitoba, you may have separate provincial sales tax registration obligations. The federal GST/HST registration does not cover these provincial taxes.

Where to Go Next

If you are setting up a Canadian small business or trying to navigate the wider compliance landscape, our Canadian Small Business Resources hub brings together the federal and provincial requirements, the CRA program accounts you will need, and the credible sources we recommend. It is the single page I send to anyone starting or scaling a business in Canada.

If you are wondering whether your current accounting setup is actually serving your growth, our Financial Clarity Assessment takes about two minutes and gives you a benchmark across the dimensions that matter for growing Canadian businesses. The Zenbooks Technology in Accounting research found that only 6% of Canadian SMEs working with an external provider receive a regular monthly check-in. If GST/HST strategy is something you have only ever discussed at year-end, that is worth knowing about your current relationship.

Eric Saumure, CPA, CA, is co-founder and Principal of Zenbooks, an online cloud-native accounting firm started in 2015 to serve 300+ Canadian small and mid-sized businesses. Before Zenbooks, Eric spent 3 years at KPMG. He specializes in financial strategy for growth-stage companies in the $1M-$10M revenue range, with a particular focus on marketing and creative agencies, SaaS, and professional services firms, e-commerce and non-profits.

Eric's commentary on Canadian small business, tax policy, and open banking has appeared in the Toronto Star, Canadian Press, CTV, CBC, Le Devoir, Policy Options, The Conversation, and Canadian Accountant. He was named to the OBJ Ottawa Forty Under 40 and recognized on both the Financial Times Americas' Fastest Growing Companies 2026 list and the Globe and Mail's Report on Business Top Growing Companies 2024. He is the principal researcher behind the Zenbooks Technology in Accounting Study, a national survey of 500 Canadian SMEs on accounting technology adoption, and the founder of OpenSME, a Canadian open banking advocacy organization. He serves on the board of Cystic Fibrosis Canada and member of the Montfort Hospital Association.

Subscribe for Updates

Business Clarity That Helps You Breathe Easy

Achieve your business goals and peace of mind with Zenbooks. As both your finance team and business advisor, we empower you every step of the way.