TOSI rules explained: a CPA's guide to tax on split income in Canada

If you own a Canadian-controlled private corporation and you're thinking about paying a dividend to your spouse, your adult child, or a family trust, the tax on split income rules decides whether that dividend gets taxed at a reasonable rate or at the highest marginal rate in the country. For most owner-managers, the difference is tens of thousands a year, and most don't realize how narrow the safe zones are. This is the plain-language walkthrough, written for owners who have to live with these rules.

What TOSI actually is

Tax on split income (TOSI) applies the highest federal and provincial marginal tax rates to certain income received by a family member from a private corporation, partnership, or trust connected to another family member who runs the business. It came into force in 2018 and replaced the narrower "kiddie tax" that only applied to minors.

The result is brutal. If an amount gets caught, the recipient pays tax at roughly 53% to 55% depending on province, with no graduated rates and limited access to most credits. That's the same rate a senior executive making $500,000 pays on their top dollar, applied to a student or stay-at-home spouse who otherwise would have paid almost nothing.

TOSI didn't eliminate income splitting. It dramatically narrowed where it works. If you fall into one of five "excluded amount" categories, you split the old-fashioned way. If not, the income gets the top rate regardless of how modest your family member's other income is.

Who TOSI applies to

The 2018 expansion pulled in adult spouses, adult children, parents, grandparents, aunts, uncles, nieces, nephews, and most family trusts where any of these people are beneficiaries. Income that can be caught includes dividends from private corporations, some capital gains on private company shares, and income from partnerships or trusts where a family member runs the underlying business. Salary paid for actual work done is not split income, and that distinction matters more post-2018 than it did before.

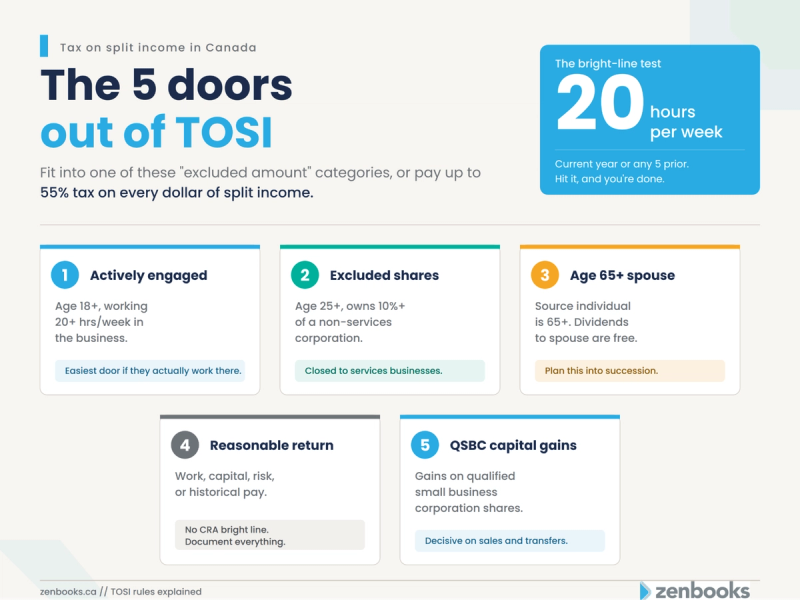

The five excluded amount tests

If an amount fits one of these five categories, TOSI doesn't apply.

1. Age 18+ engaged in the business on a regular, continuous, and substantial basis

The most misunderstood exclusion in the framework. Owners hear "engaged on a regular, continuous and substantial basis" and assume their spouse answering the occasional email qualifies. It doesn't.

The Income Tax Act gives a bright-line test. If the family member works an average of 20 or more hours per week during the part of the year the business operates, in either the current year or any five prior years (not necessarily consecutive), they automatically meet the test. Hit 20 hours, and you're done.

Below 20 hours, you lose the bright line and fall into a facts-and-circumstances test where the CRA looks at whether the involvement was still regular, continuous, and substantial. This is where most spouses of owner-managers actually sit. No formula resolves it in your favour. If the CRA asks, you're defending your facts, and you'd better have contemporaneous records.

Tara Robertson, CPA, CGA our Senior Tax Accountant, puts it this way: "The number we use internally when we're reviewing a client's structure is 20 hours a week. Not because it's a magic number, but because it's the one that lets us sleep at night. Anything less, and we're in a conversation about documentation, timesheets, and whether the involvement would read as substantial to a CRA auditor who's never met this family."

2. Age 25+ with 10% or more ownership of a non-services business

This is the "excluded shares" exemption and, in our opinion, it's underused. If the recipient is 25 or older, owns shares representing at least 10% of the votes and value of the corporation, and the corporation's income doesn't come primarily from a services business, the income from those shares is excluded.

The "non-services" restriction is where this exemption loses most of our clients. If your business is a consulting firm, a law practice, an agency, or any operation where income is substantially derived from the personal services of the principals, you don't qualify. That's a deliberate policy choice, and it's the single biggest reason excluded shares are closed to the owner-managers who could otherwise benefit most from it.

There's also a third leg of this test that catches Holdco and management corporation structures off guard. Even if the age and ownership tests are met, if all or substantially all of the corporation's income is directly or indirectly from one or more related businesses (other than a business of the corporation itself), the shares fail the excluded shares definition and TOSI likely applies. The classic example: a management company earns most of its revenue from intercompany fees billed to a related operating company, and pays a dividend to a 25-plus shareholder who owns more than 10% of the votes and value but isn't otherwise involved. The shareholder ticks the age and ownership boxes and still gets caught, because the management company is functionally living off the related Opco. If you're running a Holdco/Opco or management corp structure with adult family members on the cap table, this is the leg that will trip you up.

3. Spousal exception where the source individual is 65 or older

The quiet good-news exception almost no one plans for. If the source individual (the person running the business) is 65 or older in the year, amounts paid to their spouse or common-law partner are excluded from TOSI. It mirrors the pension income splitting rules that apply to retirees. Owners in their late 50s and early 60s thinking about succession should be modelling what their income split structure looks like starting in the year the source individual turns 65. For a couple where one spouse has no active role, this is often the first time since 2018 that meaningful dividend splitting becomes possible again.

4. The reasonable return test

Here we have to be honest with you. The test says amounts representing a reasonable return on a family member's contributions to the business are excluded. The Income Tax Act lists four factors: work performed, property contributed, risks assumed, and historical amounts paid.

What the CRA has not done, seven years after TOSI came into force, is give any meaningful numerical guidance on what "reasonable" looks like. There are no safe harbour percentages, no formula for weighting the four factors, no tolerance bands. Practitioners across the country read this test differently, and we know of cases where two reputable firms would give the same family opposite advice on identical facts.

Tara Robertson, CPA, CGA, has a line she uses in client meetings: "The reasonable return test isn't a shield. It's a defence you get to make if the CRA decides to come after you. The question isn't whether you think it's reasonable. It's whether a stranger reviewing your file in three years would agree."

Document everything, and assume you'll have to defend it. A spouse who contributed $50,000 at incorporation, kept the books for three years, and personally guaranteed the bank loan has a defensible history. If the only contribution is being married to the owner, the test won't save you.

5. Capital gains on qualified small business corporation shares

There's a specific exclusion for capital gains that would have qualified for the lifetime capital gains exemption on QSBC shares, even if the exemption isn't actually claimed. It's narrow, but for the families it applies to, it's often decisive on business sales and intergenerational transfers.

A worked example

Take a professional services CCPC in Ottawa, owned 100% by one spouse. The other spouse is 42, handles bookkeeping and bank reconciliations from home, attends the occasional client dinner, and averages six hours a week on the business. The owner wants to pay the non-active spouse a $50,000 dividend.

Walking the tests: the spouse is over 18 but works well below 20 hours a week, so the bright line fails. Six hours a week on a services file would not survive a CRA audit as "regular, continuous, and substantial." The business is a services business, so excluded shares is closed regardless of ownership. The owner is 42, so the age 65 exception is over two decades away. The reasonable return test would require arguing $50,000 is a defensible return on six hours a week of bookkeeping, a tough case.

Result: the $50,000 dividend would probably be caught by TOSI. The non-active spouse pays Ontario's top marginal rate, roughly 47.74% on non-eligible dividends at the top bracket, for about $23,870 in tax. The owner achieves no income splitting benefit. This is the structural problem TOSI creates for our typical client. The owners who most want to income split, professional services firms with one active principal and a supporting spouse, are exactly the ones the rules were designed to stop. Maybe the spouse gets a salary for their contributions that are reasonable or could be hired as an independent contractor.

The structural trap almost no one talks about

TOSI applies to the recipient, not the payer. For healthy families this is just a mechanical detail. For families that have fallen apart, it's a real problem. We've seen situations where a spouse who still owns non-voting shares from an estate freeze years earlier ends up with a TOSI-taxed dividend they never wanted, because the controlling shareholder declared a dividend on that share class. The former spouse has to pick up the income and pay top-rate tax on it. It's legal, and there's little the recipient can do after the fact.

If you're setting up a share structure involving a spouse, or doing an estate freeze that crystallizes shares to family members, the shareholders' agreement needs to address dividend declarations, not just voting rights. TOSI has made this kind of corporate structuring much more expensive to ignore.

Does TOSI apply to salary?

No. Salary paid for actual work performed is not split income. It's subject to the ordinary reasonableness test under section 67 of the Income Tax Act, and it attracts CPP and source deduction obligations, but it isn't caught by TOSI.

This has quietly created a renaissance for salary when a family member genuinely works in the business. For a spouse who does 15 hours a week of real work, a reasonable T4 salary is often cleaner than trying to argue the facts-and-circumstances engagement test for a dividend. Our Salary vs. Dividends Optimizer runs the numbers across the most common scenarios.

The honest bottom line

For owner-managers without a genuinely active spouse, without adult children over 25 in a non-services business, and without a family trust set up to solve for the 2018 rules, TOSI has largely eliminated income splitting as a lever. Not a comfortable conclusion, but accurate.

The right answer is usually to stop trying to split and focus on strategies that still work: corporate class investments for passive income, registered plan contributions, individual pension plans, holdco structures that handle passive investment income correctly, and timing dividends to tax years where the recipient genuinely has capacity. Our broader guide to reducing tax liability as a Canadian small business owner covers several of these, and our post on trusts for Canadian business owners walks through where trusts still play a role post-TOSI.

How we handle this at Zenbooks

We run roughly 300 Canadian SME files, and TOSI comes up seriously in close to half. Our approach is to flag the structure before it gets built. If a new client has a spouse shareholder, a family trust, or adult children on the cap table, the first review cycle includes a TOSI screen: who's receiving what, against which exemption, with what documentation behind it. Most problems we see were preventable two years earlier.

The infrastructure for this kind of review matters. Our 2023 technology in accounting study with Abacus Data (500 Canadian SMEs, ±4.35% margin of error) found most owners were getting a retrospective conversation at year-end rather than proactive planning during the year. That's exactly the wrong cadence for TOSI: you can't flag an issue you don't see until 14 months after the dividend went out.

The same technology in accounting research found SMEs on cloud-based, continuously-updated accounting systems were meaningfully more likely to report ongoing tax planning than those on traditional year-end cycles. Our broader research on how Canadian SMEs work with their accountants makes the point in more detail.

One long-standing client, Stefano Manzoni, wrote: "I trust Zenbooks with the set up and accounting for my Corporations. When it comes to investment properties, they know how to structure the corporate ownership." Another wrote: "Our accountant Albert is more than just an accountant for us, we consider him a family friend. He goes out of his way every year to help us {navigate} through the crazy world of taxes." I share these not to fish for compliments but because TOSI is a relationship-heavy file. The right answer depends on the family, the business, the shareholdings, and where the owner wants to be in 10 years. It's not something you solve once and forget.

Check your situation

If you're not sure whether your current structure survives a TOSI review, our TOSI Eligibility Screener walks you through the five excluded amount tests in about five minutes and tells you which ones you qualify for and where the documentation gaps are. Free to use. Same framework we run on new client files. For a broader view of the rules affecting Canadian owner-managed corporations, our Canadian small business resources hub brings together the primary CRA references, our blog archive, and our interactive tools in one place.

Frequently asked questions

Does TOSI apply to my spouse?

If your spouse receives dividends, interest, or certain other income from a corporation, partnership, or trust connected to your business, TOSI potentially applies. Whether it actually bites depends on whether any of the five excluded amount tests apply. For most non-active spouses under 65 in a services business, none of the five exclusions apply and TOSI will catch the income.

What is an "excluded amount"?

An excluded amount is income that would otherwise be split income but is carved out of TOSI by one of the five specific exemptions in the Income Tax Act: age 18+ engaged on a regular basis, age 25+ owning 10%+ of a non-services business, the age 65 spousal exception, the reasonable return test, or gains on qualified small business corporation shares.

Does TOSI apply if my spouse owns shares but doesn't work in the business?

Owning shares is not by itself a defence against TOSI. The question is whether the shares, and the income from them, fit one of the five excluded amount categories. A non-active spouse under 65 holding common shares in a services business will typically get caught if dividends are paid, even if they legally own the shares.

Can I still income split with my adult child?

Owning shares is not by itself a defence against TOSI. The question is whether the shares, and the income from them, fit one of the five excluded amount categories. A non-active spouse under 65 holding common shares in a services business will typically get caught if dividends are paid, even if they legally own the shares. The same is true if the corporation is a Holdco or management corp earning substantially all of its income from a related operating business; the excluded shares test fails on the related-business leg even when the age and ownership tests are met.

What's the difference between the kiddie tax and TOSI?

The original kiddie tax, in place from 2000 to 2017, applied only to minors under 18. TOSI, which replaced it in 2018, applies to adults as well and pulls in a much broader range of income types and family relationships.

Does TOSI apply to salary paid to a family member?

No. Salary for actual work performed is not split income. It's subject to the reasonableness test under section 67 and to CPP and source deduction rules, but it's not caught by TOSI. For family members who genuinely work in the business, salary is often the cleaner option post-2018.

Where can I read the official CRA guidance?

The CRA's technical guidance is set out in its guidance on the application of the split income rules for adults, and the underlying legislation is in section 120.4 of the Income Tax Act. Both are written for tax professionals.

Albert Park holds a Master of Taxation from the University of Waterloo and a Bachelor of Commerce from the Rotman Commerce program at the University of Toronto. He is a Chartered Professional Accountant in Canada and a licensed CPA in the State of Illinois. One of a small number of practitioners in Canada to hold both designations. His MTax research focused on GST/HST compliance and administrative design.

Before joining Zenbooks, Albert spent eight years in the tax practice at Ernst & Young (EY), where he advised clients across a range of industries on Canadian and cross-border tax matters. He now serves as Senior Tax Manager at Zenbooks, specializing in Canadian corporate tax, owner-manager tax planning, and Canadian-US cross-border structures for small and mid-sized businesses.

Albert's analysis of Canadian tax policy has been published in Canadian Accountant and Wagepoint.

Subscribe for Updates

Business Clarity That Helps You Breathe Easy

Achieve your business goals and peace of mind with Zenbooks. As both your finance team and business advisor, we empower you every step of the way.