Contractor vs employee in Canada: The CRA test, the real costs, and how to decide

You found someone you want to bring on. Now you need to decide whether to hire them as an employee or pay them as a contractor, and your gut is telling you contractor is cheaper. That instinct is wrong about half the time, and the other half it leads to the second mistake: assuming the choice is yours to make at all.

Worker classification in Canada is a facts-based determination by the Canada Revenue Agency, not a preference you express on an invoice. We will walk through the CRA's framework first, because the legal answer constrains the financial one. Then we will walk through the actual all-in cost of each path, because once you know classification works either way, you still need to know which is cheaper. That second question is where our Contractor vs Employee Cost Calculator earns its keep, and the rest of this post is the framework you need to use it intelligently.

Contractor vs. Employee True Cost

Why the trucking precedent matters for every Canadian business

You may have seen headlines in late 2025 about the CRA lifting its long-standing moratorium on T4A penalties. That change is real, but narrower than the headlines suggest. As of December 4, 2025, the CRA lifted the penalty moratorium only for the trucking industry, defined as businesses deriving more than 50 percent of primary income from trucking activities. For every other industry, the T4A reporting requirement still technically exists, but the moratorium on penalties continues. Your agency, SaaS company, professional services firm, or e-commerce business is not directly affected by the trucking change.

The reason this still matters to you is what the trucking move signals. The federal government allocated $77 million over four years to fund CRA enforcement, paired the trucking T4A change with a new dedicated Personal Services Business oversight team, and amended tax law to allow the CRA to share worker classification data with Employment and Social Development Canada. The trucking sector is the proof of concept for a broader misclassification crackdown, and the framework being built for trucking is portable to any industry where contractor abuse is suspected. Owner-operator agencies, app-based gig platforms, and any sector with high contractor density should expect to be on the radar within the next few budget cycles.

More importantly, the underlying misclassification rules have not changed. Even in industries where T4A penalties remain on hold, a CRA reassessment finding that your "contractor" was actually an employee still triggers years of unremitted CPP, EI, and income tax, plus 10 to 20 percent penalties, plus interest. The cost of getting classification wrong has always been the reassessment, not the T4A slip. The trucking change just made the reassessment easier for the CRA to find. If you are in construction, the T5018 reporting obligations have been in force the entire time and have not changed.

The CRA's four-factor test, in plain language

For most of Canada, the CRA evaluates the working relationship using the framework set out in Guide RC4110, Employee or Self-Employed. The CRA looks at the actual day-to-day reality of the relationship, not the label on the contract. There are four factors:

1. Control

Who decides how the work gets done? An employee is told what to do, when to do it, where to do it, and often how to do it. A contractor decides their own methods, hours, and location, and delivers an outcome.

A useful test: if the person works the hours your business is open, attends your team meetings, reports to one of your managers, and gets feedback on their methods rather than just their results, you are exercising employee-level control regardless of what the contract says.

2. Tools and equipment

Whose tools does the work get done on? Employees typically use the employer's laptop, software, equipment, and physical workspace. Contractors typically use their own. This factor has weakened in the cloud era because so much work now happens on shared SaaS platforms, but it still matters. A developer working from your office on the laptop you bought, with the Adobe license you pay for, is showing strong employee signal.

3. Chance of profit and risk of loss

Can the worker make more money by being more efficient, or lose money by being less efficient? Contractors set prices, manage their own costs, and bear the risk of bad estimates. If a project takes twice as long as they quoted, they eat the difference. Employees do not face this risk. Their pay is detached from project profitability.

4. Subcontracting and ownership of business

Can the worker hire someone else to do the work? Do they have multiple clients, marketing, business insurance, and the ability to refuse work? A contractor operating a real business can substitute another qualified person, advertises their services, and is not financially dependent on one client. An employee cannot send a substitute, and if you are 80 to 100 percent of their income, the CRA will treat that as integration, not independent business.

Quebec works differently

If your business or worker is in Quebec, the framework is civil law rather than common law. The CRA applies a three-step approach focused on whether a "relationship of subordination" exists, drawing on the Civil Code of Quebec. The factors look similar in substance, but the legal framing is different and Quebec courts have weighed control more heavily than the other factors. If you are hiring in Quebec, get advice specific to that jurisdiction before you finalize the arrangement.

Why the contract does not save you

The single most common mistake we see at Zenbooks is owners who think a written contractor agreement insulates them. It does not. The CRA reads the working relationship, not the paperwork. We have seen reassessments where a business was on the hook for years of unremitted CPP, EI, and income tax withholding, plus penalties of 10 percent on the first failure and 20 percent for repeat or grossly negligent cases, plus interest, all because someone wanted to skip payroll setup at the start.

The pattern that triggers this is depressingly consistent. An owner offers a candidate $80,000 as an employee. The candidate counters: "Pay me $90,000 as a contractor and we both save on payroll taxes." The owner agrees because it sounds like a win-win. It is a win-lose-lose. The owner is on the hook for misclassification penalties if the relationship has employee characteristics. The worker has no EI eligibility if the gig ends. And the CRA does not care that everyone consented. As Jessica Wong, CPA, CA and Director of Operations at Zenbooks, puts it: "Calling someone a contractor or an employee doesn't make them one. The CRA isn't reviewing the title on your agreement. They're looking at what the work actually looks like, day to day. "

We also have a Worker Classification Tool if you need help determining if someone is an employee or a contractor.

Worker Classification AnalyserWhat the cost calculator is actually for

Once you have established that a worker can legally be classified either way, the question becomes which arrangement is cheaper on a fully loaded basis. This is where most of the bad math happens, on both sides.

Hirers tend to overestimate the savings from going contractor. The instinct is: no CPP, no EI, no vacation pay, no benefits, no employer health tax, must be cheaper. But contractors charge a premium precisely because they absorb those costs themselves, plus self-employment tax overhead, plus profit margin, plus the cost of bench time between gigs, plus their own software, equipment, and insurance. When you actually run the numbers, an $80 per hour contractor working 30 hours a week and a $65,000 per year salaried employee are often within a few thousand dollars of each other on an all-in basis. The savings most owners think they are getting frequently does not exist.

Contractors, on the other hand, often undercharge. A common pattern: someone leaves a $90,000 salary, hangs out a shingle, and starts billing $50 per hour because that is roughly what their hourly equivalent was. They forget to price in unpaid vacation, unpaid sick days, the employer half of CPP they now owe themselves, the lack of group benefits, the cost of self-employed insurance, the cost of accounting and tax filing, and the four to eight weeks per year they spend selling and onboarding rather than billing. Their effective hourly cost to deliver the same lifestyle as a $90,000 employee is closer to $80 to $95 per hour. They are quietly subsidizing their clients.

The Contractor vs Employee Cost Calculator is built to answer two questions at once. For the hirer: what is my fully loaded cost either way, with the right Canadian inputs. For the contractor: what should I charge to keep the same take-home as I would in an equivalent salaried role.

Contractor vs Employee Cost CalculatorThe fully loaded cost of an employee in Canada

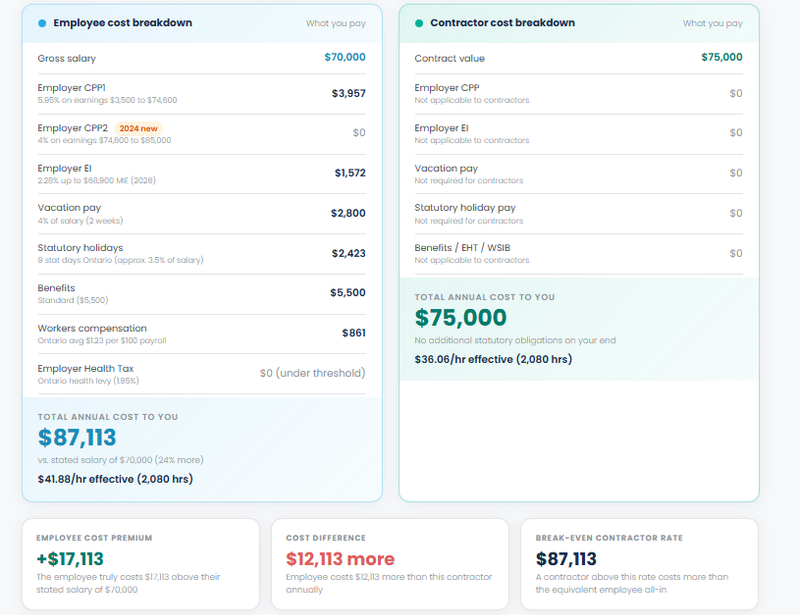

A lot of the contractor versus employee math you find online is American, and it overstates Canadian employer costs by baking in healthcare premiums and 401(k) matching that do not apply here. Canadian employer costs are real but more contained. For 2026, a fully loaded Canadian employee typically costs roughly 1.18 to 1.30 times their salary, depending on province, role, and benefits.

The components are: the employer portion of CPP, which is 5.95 percent of pensionable earnings up to the YMPE plus the additional CPP2 tier on earnings above that; the employer portion of EI, which is 1.4 times the employee rate; vacation pay accrual, which is at least 4 percent for the first five years in most provinces; provincial workers compensation premiums, which vary by industry and province; provincial employer health taxes where applicable, including Ontario's EHT for employers above the exemption threshold and Quebec's contribution to the Health Services Fund; and any group benefits, retirement matching, or perks you offer.

For a $75,000 Ontario employee at a small business below the EHT exemption, with a basic group benefits plan, the all-in cost typically runs $88,500 to $95,000. Knowing the real Canadian number, rather than the inflated American one, changes the contractor versus employee math in the employee's favour more often than people expect.

The fully loaded cost of a contractor

For the hirer, the obvious cost is the invoice. The hidden costs are real but smaller than the employee side: the time spent managing a contractor relationship, the cost of T4A or T5018 filing depending on your industry, the cost of work that has to be redone because the contractor was not embedded in your team, and the institutional knowledge that walks out the door at the end of the engagement.

The reporting obligations vary by industry. If your business is primarily construction, you owe a T5018 slip for any subcontractor paid more than $500, with penalties of $25 per day per slip up to $2,500. This has been the rule for years and is actively enforced. If you are in the trucking industry, T4A slips are now required for payments over $500 to a Canadian-controlled private corporation, with penalties of $100 per slip plus $30 per day. For every other industry, the T4A reporting requirement still technically exists, but the penalty moratorium remains in place for now. None of this is catastrophic in isolation, but the trajectory is clear. The administrative cost of using contractors is rising, and the "zero overhead" assumption that drives a lot of contractor decisions deserves a fresh look.

The case for hiring an employee, even when it is not cheaper

Owners often hire contractors to "stay lean." In practice, contractors usually make you slower, not leaner. They do not accumulate institutional knowledge. They do not show up to your team meetings. They do not care about your roadmap past the end of their statement of work. They bill you to ramp back up every time you bring them back on. And the actual fully loaded cost of a contractor includes the cost of explaining your business to a new contractor every six months when the previous one moved on.

Employees compound. Contractors do not. If you are hiring someone to do 30 hours a week of the same work for the next two years, paying contractor rates is the most expensive way to do that work, and the misclassification risk is the highest, because the relationship looks like employment to anyone with a CRA decision tree.

The right way to think about this is not "contractor or employee." It is: what is the smallest commitment I can make to get this work done well. Sometimes that is a contractor for a defined project. Sometimes it is a part-time employee. Sometimes it is a fractional executive. Sometimes it is an agency. The calculator's job is to make the cost trade-off legible across all these options.

What good advisors actually do at this decision point

Hiring decisions are not just tax decisions. They shape your operating model for years. Oliver Wolf, Co-Founder and Director of Beyond the Peak Inc., a professional services firm Zenbooks works with, shared a Clutch review describing the kind of trust and impact a outside firm can provide: “I super appreciate their consistency and how much I can trust them with the things I need.” You can read the Beyond the Peak review and others on our Clutch profile.

That kind of advice is also what the Zenbooks Technology in Accounting study identified as a structural gap across Canadian SMEs. Of the 500 Canadian small and mid-sized businesses surveyed, only 32 percent reported satisfaction with their accountant's strategic input, and the gap between the analysis owners wanted and what they were actually getting was wide. Hiring decisions sit squarely in that gap.

Some context on the Canadian hiring market in 2026

About 2 million Canadians are self-employed, representing roughly 13 percent of total employment, a share that has stayed remarkably stable for a decade. Statistics Canada's most recent data shows that 71.9 percent of self-employed workers have no employees, and 26.6 percent of self-employed workers meet the definition of "gig workers", short-hours, no premises, no stable client base.

For owners hiring in 2026, two things follow from this. First, there is a deep pool of legitimate contractors, people running real businesses with multiple clients and their own infrastructure. Second, the gig-worker share is exactly the population most likely to fail the CRA classification test, because they often lack the multi-client, business-investment characteristics that distinguish a contractor from a disguised employee. If your "contractor" is doing 100 percent of their billable hours for you, they are statistically in the high-risk zone for reclassification.

A worked example

You need 30 hours a week of marketing operations work for the next 18 months. A senior marketing ops candidate quotes you $85 per hour as a contractor, working from her home office, on her laptop, with two other clients. Annual cost: $85 times 30 hours times 50 weeks equals $127,500.

The same candidate would accept a $95,000 salary for a permanent full-time role with benefits. Fully loaded at 1.22 times salary: $115,900.

On paper, the employee is $11,600 cheaper per year. But she is asking for full-time and you only need 30 hours, so the right comparison is $95,000 times 0.75 for a part-time employee equals $71,250 base, fully loaded at $86,925.

The part-time employee is now $40,575 per year cheaper than the contractor. The contractor only wins if the work is genuinely bursty or if the candidate cannot be retained at part-time. This is the kind of analysis the calculator surfaces in 30 seconds, and it routinely changes the decision.

Contractor vs Employee Cost CalculatorHow Zenbooks helps clients work through this

For our clients, the contractor versus employee question typically comes up at three moments: the first hire after the founder, the scale-up moment when the team crosses 10 people, and the post-acquisition restructuring moment. At each, the answer is different, and the cost difference between getting it right and getting it wrong is usually in the tens of thousands of dollars.

What we provide is the same controller-level support that helped Sterling Sky grow from 5 to 40-plus employees, and that helped Moniker Partners scale from $5M to over $20M in four years. The work is part tax, part operations, part workforce planning. If you are at one of those inflection points, the cost calculator is a good starting point, but it is the conversation about which arrangement actually fits your operating model that turns the right number into the right decision.

Frequently asked questions

Can I just hire this person as a contractor if we both agree?

No. The CRA assesses worker classification based on the actual working relationship, not on what you and the worker agree to call it. A written contract is evidence of intent, but it does not override the facts. If the working relationship has employee characteristics, the CRA will reclassify regardless of consent.

What happens if the CRA reclassifies my contractor as an employee?

The business becomes liable for the unremitted CPP and EI contributions, including both the employer and employee portions if they cannot be recovered from the worker, plus income tax that should have been withheld. Penalties start at 10 percent of the unremitted amounts and rise to 20 percent for repeat or grossly negligent failures. Interest accrues from the original due dates. Reassessments commonly cover the past three years.

If I am unsure how the CRA would classify a worker, can I get a ruling in advance?

Yes. Either the worker or the payer can request a CPP/EI ruling from the CRA by filing Form CPT1 or through the Represent a Client portal. The CRA will issue a written determination based on the facts. Rulings can be requested up to June 29 of the year following the year in question. If you are setting up a non-obvious arrangement, requesting a ruling at the start is cheaper than litigating a reassessment later.

Do I need to file a T4A for every contractor I pay?

It depends on your industry. If your business is primarily in trucking (more than 50 percent of primary income from trucking activities), as of the 2025 tax year you must file T4A slips reporting payments over $500 to Canadian-controlled private corporations, with penalties for non-compliance. If your business is primarily in construction, payments over $500 to subcontractors go on a T5018 slip, and this has been actively enforced for years. For all other industries, the T4A reporting requirement technically exists in legislation, but the CRA has had an administrative moratorium on penalties for failing to file box 048 since 2011. That moratorium remains in place outside of trucking as of April 2026. The trucking change is widely expected to be a precedent, so businesses with significant contractor spend should consider voluntarily filing T4As now rather than waiting for the moratorium to lift in their industry.

Is paying a contractor through their incorporated business safer than paying them personally?

It is safer for some risks but not all. If the worker invoices through their own corporation, the relationship between you and the corporation is generally a business-to-business relationship. However, the CRA can still apply the Personal Services Business rules, which treat a corporation as a disguised employee if the individual would reasonably be considered your employee in the absence of the corporation. PSB classification carries its own punishing tax consequences for the contractor's corporation, including a higher tax rate and the loss of most deductions. If your "contractor" works for you full-time through their HoldCo and has no other clients, PSB risk is real.

Can the same person be both an employee and a contractor for my business?

It is possible but uncommon, and the CRA scrutinizes these arrangements closely. The two contracts must be genuinely separate and distinguishable, with different work, different terms, and different operational realities. If the work is the same and only the labelling differs, the CRA will treat both as employment. If you are considering this, request a CRA ruling first.

What is the cheapest way to bring on someone for short-term work without misclassification risk?

For genuinely short-term, defined-scope work, hiring through an established agency or hiring an incorporated contractor with multiple clients is generally the cleanest path. For ongoing work, a part-time or fractional employment arrangement is often cheaper than people expect, and removes the classification risk entirely. But I would also point to the roughly 90 day probation period in most provinces that allow termination of employment without any severance or termination pay.

How does the cost calculator handle provincial differences?

Our calculator accounts for the provincial variations that actually move the number: workers compensation rates by province and industry, employer health taxes where applicable, and provincial vacation accrual minimums. For Quebec, it adjusts for the QPP and QPIP in place of CPP and EI. The calculator gives you a defensible all-in number for your province, not a national average that does not match anywhere.

The bottom line

Hiring decisions in Canada are constrained first by the CRA's classification test and then by the economics. Skip the first step and you risk a reassessment that will dwarf any savings the calculator showed you. Skip the second step and you will hire the wrong type of worker for the work you actually need done.

The 2026 T4A reporting changes have raised the stakes on getting this right. The good news is that the framework is knowable, the math is calculable, and the path from "I think I should hire someone" to "I have hired the right kind of someone" is shorter than most owners assume. The calculator is the second step. The CRA test is the first. Take them in order.

Have a hiring decision on your desk right now? Run the numbers in our cost calculator, then book a 30 minute call if you want a second pair of eyes on it.

Jessica Wong, CPA, CA, is Director of Operations at Zenbooks, where she has led the firm's accounting services and client operations since 2020. She brings over a decade of experience working directly with small and mid-sized business owners, with a focus on building efficient financial processes, improving month-end close cycles, and translating complex numbers into clear operational insights.

Before joining Zenbooks, Jessica held senior accounting roles across the hospitality and professional services sectors, including Corporate Controller at Hawksworth Restaurant Group and Manager of Client Onboarding at a national cloud accounting firm. She began her career in public accounting at Crowe. She holds a Bachelor of Business Administration from Simon Fraser University and her CPA, CA designation.

Jessica's writing on accounting operations and the future of remote work has appeared in the Toronto Star.

Subscribe for Updates

Business Clarity That Helps You Breathe Easy

Achieve your business goals and peace of mind with Zenbooks. As both your finance team and business advisor, we empower you every step of the way.